During COVID-19, it’s critical for business owners to make decisions based on empirical data, especially if they’re considering a sale of their business.

Key insights

- While COVID-19 has triggered market turmoil, history shows that the U.S. stands ready to support our economy on both a fiscal and monetary basis.

- Private equity funds continue to grow in both number and capital overhang.

- Companies that perform well through the COVID-19 shock could demand a premium valuation in the market.

- M&A volume may expand dramatically as Baby Boomers, fatigued with yet another significant shock to the market, move to divest their businesses.

There is no shortage of headlines and soundbites that suggest the current COVID-19 pandemic has triggered an economic calamity, leaving many business owners to believe we are entering a recession much like the one we saw in 2008 – 2009. This creates a scenario where business owners are left to decipher between what is true and measurable versus what is political — and even clickbait-motivated — rhetoric.

Need help navigating the current M&A environment?

Are these headlines truly based on measurable, empirical market data or on what history has taught us about federal responses to past economic retreats? The answer to this question is particularly important for M&A markets and for business owners faced with a sale of their business. Let’s put the current COVID-19 shock into perspective by stepping back to examine the empirical data and the qualitative realities found in U.S. fiscal and monetary policy history.

A look at history

Are we heading toward an economic depression — perhaps one similar to, or even worse than, the Great Depression of the 1930s?

Barring some additional once-in-a-generation shock to the system, and based on the historical evidence, we believe the history and empirical data suggest the answer to this question is no. We are not heading toward a Great Depression version 2.0. A proactive Federal Reserve (the Fed), in tandem with swift fiscal stimulus, have substantially decreased, if not eliminated, the risk of an economic depression.

Monetary policy

Since the days of Fed Chair Paul Volcker in the 1980s, the institution has adopted policies and used procedures to keep inflation in check and keep the U.S. economy at a “natural level” of unemployment. While some of these tools were weakened during the Great Recession of 2008 – 09, the Fed still maintains numerous weapons to perform its job effectively.

As the Fed’s role relates to the possibility of a depression, critics of the institution continue to forget that today’s Federal Reserve has the benefit of hindsight with respect to actions taken during the Great Depression. Among the macroeconomic views of the Monetarist and Keynesian schools of thought, there seems to be consensus that a number of the policy actions taken by the Fed in the late 1920s and early 1930s did little to alleviate economic conditions during the Great Depression.

While these two macroeconomic theories continue to differ on the Fed’s role in and the key drivers of economic growth, both agree that the restrictive monetary policies undertaken by the Fed (such as increasing interest rates in 1928 and 1929) contributed significantly to deepening and lengthening the Great Depression. Both schools also agree that policies to expand the supply of money could have shortened the Great Depression. In the field of macroeconomics, it is one of the few areas that both schools of economic thought agree.

We believe that the claims that a depression is on the immediate horizon are, at best, misguided as critics seem to forget that the Great Depression was a hard lesson learned for the Fed, and the actions have not been repeated since. The U.S. economy did not experience a depression after the stock market shocks of 1987, the tech bubble burst of 2000, the precipitous drop of the market after 9/11, or even after the great loss of wealth experienced from the real estate crisis during the Great Recession.

Today’s Fed has been swift to expand access to money and credit. It has eased borrowing costs, implemented quantitative easing, and provided lending facilities to small- and mid-sized businesses through its Main Street Lending Program. The Fed has consistently demonstrated that it “learned its lesson” during the Great Depression and that it remains a powerful — if not the most powerful — tool for U.S. markets to avoid economic calamity.

Fiscal policy

With respect to fiscal policy, the U.S. government remains willing and able to provide stimulus packages to counteract the fallout from COVID-19. While a stimulus of $2.4 trillion seems enormous in the context of dollars allocated to a government stimulus, the chart below demonstrates that these dollars, taken as a percent of GDP, make the current stimulus much more akin to the packages provided during the recessions of the mid-1970s and early 1980s. To date, Congress has enacted an economic stimulus approximating 11.5% of GDP, far below the stimulus during the Great Depression, and below the stimulus after 9/11 and during the Great Recession of the late 2000s.

New data also suggests that the relief provided by Congress may be in surplus to the current needs. Recent figures from the Small Business Administration (SBA) demonstrates that the demand for financial relief for small businesses has decreased since the initial round of Economic Injury Disaster Loan (EIDL) and Paycheck Protection Program (PPP) loan offerings. The second round of offerings, comprising more than 2 million loan approvals, had an average loan size of $79,000 compared to an average loan size of $206,000 during the initial round (Sources: SBA Paycheck Protection Program (PPP) Report and SBA Paycheck Protection Program (PPP) Report: Second Round).

Furthermore, only 7,600 loans approved in the current second round exceeded $2 million when compared to more than 26,000 approved loans above $2 million in the initial round (Sources: SBA Paycheck Protection Program (PPP) Report and SBA Paycheck Protection Program (PPP) Report: Second Round). While some of these decreases can be attributed to certain provisions of taking these loans and the mix of businesses now applying for these loans (more proprietorships and small contractors), the reduction is noteworthy.

A review of recent market performance

Since the introduction of COVID-19 activity in the equity markets, equity investors and the greater markets have not only viewed the current monetary and fiscal policies favorably, but the empirical data signals favorable expectations for the economy as it opens up and people return to work.

On February 19, 2020, the S&P 500 peaked at a level of 3,386. By March 23, the index had bottomed out at a level of 2,237 (a 33.9% decline). As of the close of trading on May 15, the index has climbed back to a level of 2,864, a level 28% higher than the March 23 low and 15.4% below the peak of February 19. In other words, as of May 15, the S&P 500 has gained back over half of its losses since its peak on February 19.

(Source: www.capitaliq.com)

Furthermore, on a year-to-date basis, through May 15, the S&P 500 index has only declined 12.1% (Source: www.capitaliq.com). That level of drop followed by recovery is not consistent with an imminent depression; it is much more in line with levels consistent with a market correction, which is not unusual after a decade-long bull market.

The Dow Jones Industrial Average (DJIA) has followed much of the same pattern as the S&P 500. On February 12, 2020, the DJIA peaked at a level of 29,551, and by March 23 the index had bottomed out at a level of 18,592 (a 37.1% decline). As of the close of trading on May 15, the index has climbed back to a level of 23,685, which is 27.4% higher than the March 23 low and 19.9% below the peak of February 12.

(Source: www.capitaliq.com)

The DJIA has gained back nearly half of its losses since its peak on February 12. On a year-to-date basis, through May 15, the DJIA has declined 18.0% (Source: www.capitaliq.com). Again, this is far from what you would anticipate if a depression were looming.

A review of recent market volatility

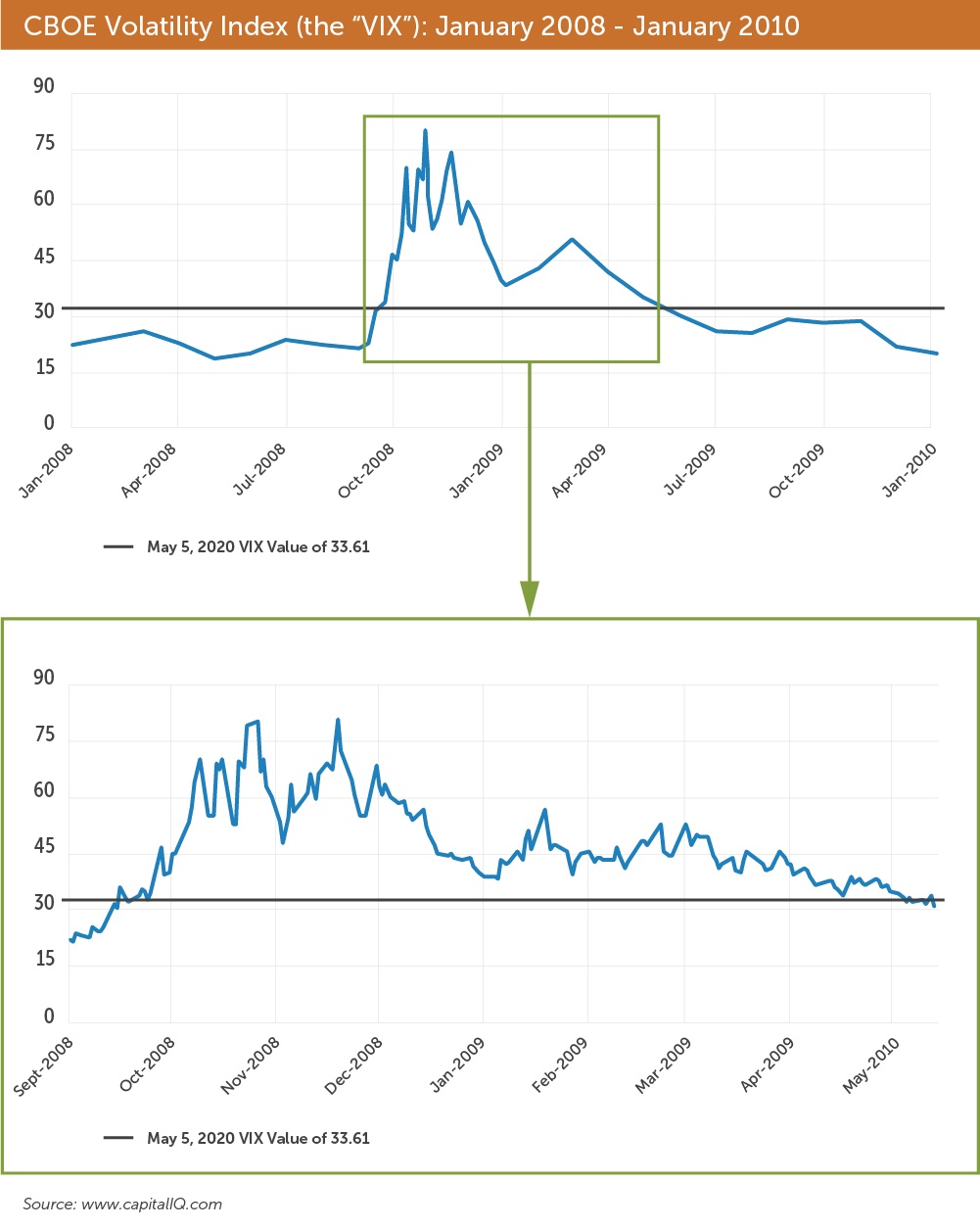

The CBOE Volatility Index (the “VIX”), a measure of market volatility, has also shown favorable trends. When the equity markets began to price in the economic impact from COVID-19, the VIX peaked at 82.69 on March 16, 2020. As of May 15, the index stood at 31.89, a decline of over 50 points. To put that in historical context, the VIX has averaged 16.42 since the beginning of 2015.

(Source: www.capitaliq.com)

The recent declines in the VIX since the initial shock suggests not only that uncertainty is abating in the markets, but that this uncertainty is abating quickly. As of the date of this article, we are now facing a financial backdrop of recovering markets and reduced volatility. These are not only positive signals for U.S. economic health, but positive signals for the M&A markets that are closely correlated to public market activity.

Furthermore, when you empirically examine the VIX and its movement during the Great Recession, market volatility was spread over a much longer extended period than it is currently. During the Great Recession, the VIX peaked at 80.86 on November 20, 2008, and did not return to May 15, 2020 levels of 31.89 until May 12, 2009 (173 days later).

(Source: www.capitaliq.com)

When the shock of COVID-19 went through equity markets, the VIX spiked to levels not seen during the Great Recession; however, the recent rapid decline in the VIX, compared to the decline in the VIX during the Great Recession, demonstrates that investors view the impact of COVID-19 as akin to a natural disaster or a one-time economic shock, rather than a structural, systemic flaw in the economy. This empirical data suggests the current COVID-19 crisis does not bear similarity to the Great Recession when the market is examined from a volatility perspective.

The current health of the U.S. banking system

A reasonable question for any seller or M&A practitioner to ask is, “What about the banks?” Business owners, investors, and, frankly, all citizens remain traumatized by a flawed — and in many cases, failed — banking system during the Great Recession that required an unprecedented taxpayer bailout.

Subsequent to the Great Recession, much has changed in the banking system. First, banks are not peddling mortgage bonds with AAA credit ratings that actually comprised subprime loans. Additionally, legislation and penalties implemented after the Great Recession, along with increased capital requirements for U.S. financial institutions, has resulted in well-capitalized banks that are more resilient to economic shocks and exposures than they were in 2008.

At the end of 2019, the ratio of nonperforming loans to total loans, as well as net charge-offs, stood at decade lows of 0.91% and 0.52%, respectively (Source: fool.com, citing data from the Federal Deposit Insurance Corp.). While real estate prices appear inflated, particularly in the urban multifamily housing sector, banks are much more resilient to their underwriting standards, and loans that are not initiated in the traditional banking system are under much more scrutiny than they were in the run up to 2008.

Furthermore, bank reserves during 2008 stood at approximately $44 billion (Source: Asset Preservation Incorporated). Today, these reserves stand at $1.7 trillion (approximately 38 times larger), suggesting that banks are well-equipped with the capital to withstand COVID-19 and provide financing to borrowers (Source: Asset Preservation Incorporated).

With the guarantee by the Federal Reserve to purchase PPP loans from financial institutions, bank balance sheets will not be burdened with PPP debt and bank reserve requirements should remain relatively unaffected. In addition to the positives of the current banking sector, our economy entered 2020 fundamentally healthy. Unemployment was below 4%, nominal GDP was in the 3-4% range, corporate profits approximated $2.1 trillion (compared to $700 billion in 2008), and corporate cash approximated $1.3 trillion (compared to $200 billion in 2008) (Source: Asset Preservation Incorporated).

In the context of the M&A markets, the banks are well-capitalized and are still “open for business” to provide financing for M&A transactions. While in the last month they have been, in large part, distracted placing PPP loans, they are in no way closed to lending on M&A transactions as many banks were during the worst parts of the Great Recession.

Borrowing costs

While borrowing costs have increased in light of the pandemic, there is little evidence to suggest that increased borrowing costs will significantly stunt M&A transactions or cause prospective buyers to pull back because of the prospect of more expensive debt. While the price of borrowing can influence the prices paid by financial buyers more so than their strategic counterparts, financial buyers still have a considerable overhang of $1.5 trillion in funds that they must deploy (Source: cnbc.com, Rooney, K. [2020, January 3]. Private equity’s record $1.5 trillion cash pile comes with a new set of challenges).

Furthermore, with the explosion in the number of private equity groups and the volume of transactions they perform, private equity has become a much more significant industry in the U.S. and, as a result, may weaken the strong correlation between M&A deals closed and interest rates. As shown in the chart below, consider the years 2004 and 2019, when one-year LIBOR averaged approximately 2.25%, and the bank prime loan rate averaged between 4.75% and 5.0% (Source: www.capitaliq.com, St. Louis Federal Reserve).

During these two periods, borrowing costs were similar, yet the number of closed transactions in 2019 was nearly double the number of closed transactions in 2004. This can be attributed to the number of private equity groups and their associated capital overhang (funds raised that have yet to be deployed). In 2000, there were approximately 1,500 private equity groups; in 2019 there were over 5,000 (Source: www.pitchbook.com). Of course, if the Fed raised the federal funds rate to Paul Volcker’s early 1980s levels of 20%, there would be a significant slowdown in transactions closed. But this is not the early 1980s and the U.S. is not fighting 10% annual inflation rates. A rise of a few basis points should not concern business owners that the M&A markets are inactive.

Conclusions to consider

With these realities in mind, there are a number of conclusions that we believe are important to consider during the COVID-19 era:

(1) While COVID-19 has triggered market turmoil, history shows that the U.S. stands ready to support our economy on both a fiscal and monetary basis. Fiscally, the current stimulus programs are more akin to the recession stimulus plans of the mid-1970s and early 1980s, when put in the perspective of our nation’s GDP. From a monetary policy standpoint, the Fed still retains many useful tools to support economic growth.

When the empirical market data is examined, the pullback financially resembles much more of an economic correction from a 10-year bull market. The S&P 500 and the DJIA have declined only 12% and 18% year to date, respectively, and the volatility in the markets is substantially declining since they peaked in March (Source: www.capitaliq.com). These statistics do not support that we are on the brink of a depression. Rather, it could be argued that we may be at the beginning of another bull market after a much needed market correction.

(2) Private equity funds continue to grow in both number and capital overhang. Private equity funds now have an estimated $1.5 trillion in overhang compared to just over $500 billion only 10 years prior (Source: cnbc.com, Rooney, K. [2020, January 3]. Private equity’s record $1.5 trillion cash pile comes with a new set of challenges). These funds are meant to deploy their capital quickly in hopes of earning a great return, which then allows the private equity fund’s general partners to raise more funds for future investments. The availability of private equity funds that are yet to be deployed cannot be overlooked, especially as interest rates remain historically low.

(3) Companies that perform well through the COVID-19 shock could demand a premium valuation in the market. While there is likely to be decreased breadth of bidders and decreased “outlier” bids for standard businesses, if you have a business that has demonstrated the ability to resist the economic fallout from COVID-19, buyers may be more willing to transact. Add in the competitive tension that an investment banker brings to the M&A process, and these sellers in particular may achieve enhanced valuations.

For the more standard businesses that have some displacement, lost sales, or increased costs related to COVID, the expectation of receiving a “fair price” if you hire an investment banker may need to be reset. On one hand, the M&A market is coming off five years of a seller’s market and the music had to stop at some point. On the other, the M&A market continues to have strong fundamentals, large cash reserves, and many buyers competing for a limited number of deals. Only time can tell what the future holds for these businesses.

(4) Sellers will need to capture and track all extraordinary costs and conservatively estimate lost sales resulting from COVID-19. These will be critical adjustments to EBITDA that, with adequate support and rationale, could be favorable to sellers.

(5) In the near term, purchase price proposals from buyers may comprise various contingent financial instruments to bridge the gap between seller and buyer valuation expectations. While an all-cash deal is always preferred, negotiations are likely to be more fluid as the market corrects. Anticipate more proposals with earn-outs, seller paper, and other contingent payments. We always recommend that owners retain an investment banker to negotiate on the seller’s behalf to consider these contingencies.

(6) M&A volume could expand dramatically as Baby Boomers, fatigued with yet another significant shock to the market, may move to divest their businesses. This demographic driver is often the least recognized, but we believe may provide the greatest growth to M&A markets for years to come. An estimated $30 trillion in wealth resides with Baby Boomers born between 1944 and 1964 (Source: cnbc.com, Sigalos, M. K. [2018, July 10]. $30 trillion is about to change hands in the US). The COVID-19 pandemic, combined with other economic downturns that Baby Boomers experienced in preceding decades, will likely help to expedite sales of businesses and M&A activity, along with a great transfer of wealth to younger generations.

While current business headlines associated with the COVID-19 pandemic can suggest an economic calamity or even an impending economic depression, the historical and empirical evidence currently does not support those conclusions. If anything, the data suggests that the economy deliberately froze and markets reacted to a short period of unknowns. Using the markets as a barometer for the greater M&A market, we anticipate a robust bounce back driven by a loosening population, continued favorable lending terms, all driven by an underlying Baby Boomer generation who may conclude that now is the time to sell.

How we can help

COVID-19 has caused great uncertainty, which makes it critical to work with financial professionals who can review historical and empirical evidence to help you chart a path forward. At CLA, our team can help business owners navigate the current M&A market, whether you’re looking to buy or sell.