Good afternoon, everyone. Thank you for joining us again on our CLA Outlook for the second-half of 2026. I'm joined with Chris Dhanraj. We're going to walk through an update.

What we wanted to start off with here is, what are the top five risks that business owners and investors are faced with right now?

If we look at kind of really three key highlights that we're going to dig into here, one is that the economy is slowing, but it's not breaking. And there's a phrase that we think is appropriate here, that this is late-cycle expansion, not a recession.

So we continue to see the economy grow and that's a positive.

The second key point, we've used this phrase for several quarters now that it is “higher for longer” as it pertains to interest rates. We're seeing it both in the 10-year and the 30-year Treasury, we're seeing it in both Fed funds rate, but this is definitely an era of rates being higher for longer.

And then finally, AI is the really primary growth driver right now.

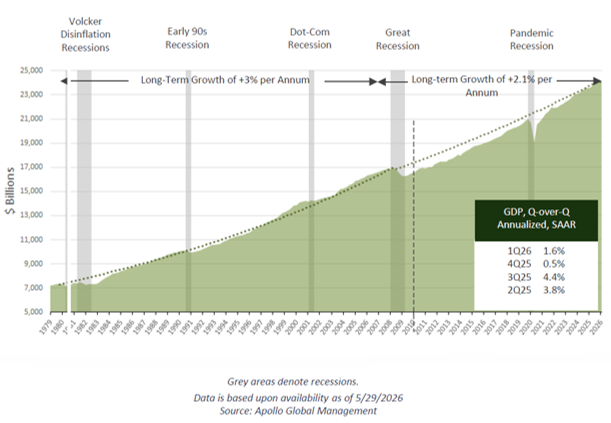

So what we're seeing here on the chart is a long-term progression of where GDP has been in the United States. And if you look at that bottom box on the bottom right, what you're seeing is actually GDP growth by quarter.

So certainly last year you had some very strong GDP numbers.

And part of the reasonings behind this slowdown GDP growth, one is the government shutdown and there's other things that people are looking at, which is the unwind of tariffs and other types of one-off types of things.

But it is appearing that GDP growth is slowing. However, it's still positive.

And when we talk about, What is a recession? A recession is two consecutive quarters of negative GDP growth.

We're not seeing that. We're seeing slowing growth perhaps, but not negative growth.

So what are we seeing as areas that are contributing to GDP growth, Chris?

Well, certainly because of the unwind of tariffs, you're actually seeing negative tariff impacts to the U.S. economy. Right? So exports, for example, and that exports, which is the difference between imports and exports, have actually been a drag to the economy.

Consumption, the consumer, we've talked about being 70% of GDP has remained quite robust, but it's actually pulling back quite a bit.

The biggest contributor in the positive side to the economy is really two interesting things.

One is government spending and then the other one is business fixed investment. Think about investment in manufacturing and other pro-business things that have happened.

So you're seeing a bit of a mixed bag where maybe tariff positive impacts are rolling off, but then you're seeing a replacement with business fixed investment and also government spending.

Also contributing to the measurement of increased inflation growth. Yeah, a big piece of this is this Iran conflict and you see this near-term rise in inflation that is really just in the last three months.

We were trending lower, but this Iran conflict is certainly something that from that geopolitical risk standpoint, the hope is that that would subside.

But I want to highlight one other data set on here. If you look at the top right corner, the box that shows stocks bond 60/40 portfolio and this is the annual average total return going back 75 years: Stocks being 11.7, bonds being 5.2, and a 60/40 portfolio being 9.4.

The crazy thing is the compounding effect over 20 years.

When you look at the growth of 100,000, just that simple additional 2% a year of 100% in equities is nearly a 50% increase in your total value of the portfolio because that's 908,000 versus a 606. So it is, it is massively impactful.

What our takeaway would be in recommendation to clients is always like, stay invested, invest for the long term, continue to rebalance and, and invest accordingly with what your financial plan and goals are.

So key opportunities for business owners, where are we looking to really advise and help take advantage of some of the current opportunities: leveraging AI and automation to expand capacity and reduce cost.

There's no doubt about it. We continue to see this expansion, Chris, across public companies and their earnings growth and this continued opportunity of productivity gains.

So the other component would be explore selling your business as valuations across industries remain elevated. We continue to see significant demand from private equity across the privately held business space.

I'd say in large part what we're noticing is that the valuation of these companies, when we say remains elevated, they are significantly higher than where they were five years ago.

And as you mentioned, Chris, the One Big Beautiful Bill benefits this 100% bonus depreciation, the immediate R&D expensing and credits, and then the Opportunity Zone extension.

So when you look at what we're telling investors right now, I think we need to keep widening our apertures, right? It's not just stocks and tech stocks only.

We want to have a diversification across stocks, across regions, across sectors, and across dividend-paying stocks as well.

I think for bonds — we mentioned this, you know, several times here — bonds are really attractive right now. The yields and the ability to lock in 5% or more is very attractive for a client base that's living longer and longer and longer.

And then lastly, alternatives can and do play an important part of the portfolio, but one of our extensive due diligence items that we look at is the amount of leverage that certain alternative managers take. You see this in the private credit space, you saw this prior in the private real estate space during the downturn.

Watching how much leverage you are taking within your alternative manager matters a lot.

Well, we appreciate everybody joining us. Chris, thank you. As always, look forward to seeing how things play out. Thank you everybody.

Key insights

- The economy is slowing, but growth remains intact; this is a late-cycle expansion, not a downturn.

- Interest rates are likely to stay elevated longer than expected, reshaping borrowing and investment decisions.

- Inflation remains uneven, with recent geopolitical pressures adding near-term volatility.

- AI-driven investment and productivity gains are becoming a major force behind earnings and business spending.

- Capital markets are shifting, creating new opportunities in fixed income, diversification, and strategic transactions.

Plan smarter with economic and market outlook signals.

Six months into 2026, the economic picture has shifted. Growth is slowing, yet the economy continues to expand. Inflation was expected to ease, yet it’s proving more resilient. Markets anticipated rate cuts, but expectations have flipped. At the same time, capital continues to flow into both equities and fixed income.

For business owners, investors, and operators, the question is: What does this mix of signals mean for your next move? Here’s where the economic and market outlook is crystallizing and how to think about it.

A slowing economy that’s still growing

Economic growth has clearly decelerated from the strong pace of 2024 – 2025. Recent GDP readings show slower expansion, but importantly, growth remains positive.

While consumer spending has eased from its peak, increased government spending and business investment are helping sustain overall economic expansion.

This is not a contraction environment. Instead, we’re in a late-cycle phase where momentum is cooling but still intact. Manufacturing and services activity continue to expand, and business sentiment, especially among small and mid-sized organizations, remains steady.

What this means for you:

- Demand may normalize, but it hasn’t disappeared

- Planning should shift from rapid growth to measured execution

- Cost discipline and margin management become more important than top-line acceleration

At the same time, the gap between perception and reality is widening. Consumer sentiment remains subdued, largely due to affordability pressures, even as underlying business activity holds up.

We talked about the economy certainly slowing, and so what is actually in the negative and what is positive? Well, certainly because of the unwanted tariffs, you're actually seeing negative tariff impacts to the U.S. economy.

On Trade, net exports which is the difference between imports and exports, have actually been a drag to the economy. Consumption, the consumer we've talked about, being 70% of GDP has remained quite robust, but it's actually pulling back quite a bit.

The biggest contributor on the positive side to the economy is really two interesting things; one is government spending and then the other one is business fixed investment, think about investment in manufacturing and other pro business things that have happened.

So, you're seeing a bit of a mixed bag where maybe tariff positive impacts are rolling off, but then you're seeing a replacement with business fixed investment and also government spending.

“Higher for longer” interest rates are now the base case

At the start of the year, markets expected rate cuts. That outlook has reversed. Persistent inflation and recent geopolitical shocks have changed the trajectory.

Instead of easing policy, the Federal Reserve is now expected to hold rates higher for longer, with increased probability of additional tightening. This shift carries real implications across the business landscape.

What this means for you:

- Borrowing costs are likely to remain elevated, affecting capital decisions

- Long-duration investments require tighter return discipline

- Cash management strategies matter more than they have in years

It also reinforces a broader reset: the low-rate environment that defined the past decade is no longer the baseline. Planning assumptions should reflect that change.

Want to explore more about the impact on your portfolio or business? Watch the video.

Inflation isn’t trending in a straight line

Inflation appeared to be moderating earlier in the year, but that trend has stalled. Energy prices, influenced by geopolitical tensions, have driven a recent surge. Because inflation is increasingly tied to global events, it creates an uneven operating environment for businesses.

What this means for you:

- Input costs may remain unpredictable, especially for energy-sensitive industries

- Pricing strategies need flexibility, not fixed assumptions

- Budgeting should account for volatility, not just directional trends

The broader takeaway: Inflation may still ease over time, but the path will likely be indirect.

AI investment is driving growth and changing the market

One of the clearest themes emerging this year is the scale of AI-driven investment.

Capital expenditures tied to AI infrastructure and technology are accelerating, contributing meaningfully to economic growth. This is showing up in earnings, productivity gains, and business investment trends.

It also explains a key dynamic in equity markets: While a handful of large technology companies have led performance, earnings growth is now broadening beyond that group.

There has been a narrative the past couple years that money flowing into equities has really been really focused on technology companies. And you talk about the Mag Seven, which are NVIDIA, Apple, Microsoft, Google, or Alphabet, Amazon, Tesla, and Meta.

These companies have actually become something like 35 to 36% of the index because of their rapid acceptance as growth drivers within the U.S. equity market. And so what we did here is we broke apart the earnings growth from Mag Seven companies versus the other 493 non-Mag Seven companies.

What it tells you is that certainly the past couple years we've seen a lot of strong growth from the Mag Seven companies. Should be no surprise, these companies are in the news all the time, but they've been growing something like 30%, 35% a year.

What I think is really interesting, however, is that non-Mag Seven companies have actually continued to grow as well. They are using AI or optimization to continue to make their businesses more profitable, and therefore their earnings are growing at the highest level since 2021.

So, one of the things that we're seeing here is that as we move forward, it's not that equities by itself are expensive or not expensive. It's when you drill deeper, finding those areas that perhaps don't have those elevated valuations like those non-Mag Seven companies, dividend paying stocks, international stocks, small cap stocks, all areas which have more attractive valuations than some of the more expensive parts of the market.

What this means for you:

- AI is shifting from experimentation to operational impact

- Productivity investments are becoming a competitive differentiator

- Growth opportunities are expanding beyond large-cap technology

Capital markets are resetting and creating new opportunities

Markets are adjusting to this new environment in real time. Stocks remain elevated, supported by earnings growth. At the same time, bond yields have risen to levels not seen in years, making fixed income a more compelling option for income and capital allocation.

This creates a more balanced opportunity set than we’ve seen in the past decade. Key shifts to watch:

- Stocks — Growth continues, but valuations suggest a more moderate pace

- Bonds — Higher yields make income strategies more attractive

- Market leadership — Performance is broadening beyond a concentrated group of companies

For business owners, there’s a parallel dynamic playing out: Valuations across industries remain elevated, driven in part by capital availability and private equity demand.

What this means for you:

- Revisit portfolio and capital allocation strategies: diversification matters more

- Consider fixed income not just for stability, but for income generation

- For owners, this may be a window to evaluate transition or liquidity strategies

How CLA can help with financial planning

In a market defined by mixed signals, clarity comes from connecting the economic outlook to your specific situation.

CLA teams work with businesses and investors to:

- Assess how macroeconomic trends affect your industry and strategy

- Identify opportunities to leverage technology and improve productivity

- Support transaction planning, including succession and exit strategies

- Evaluate capital allocation, liquidity, and financing decisions

- Align tax planning with evolving legislation and incentives

Contact us

Plan smarter with mid-year economic and market outlook signals and adjust your strategy for 2026 market shifts. Complete the form below to connect with CLA.