Key insights

- Evolving funding arrangements can make nonprofit revenue recognition more complex — and getting the accounting model right starts with understanding the nature of each transaction.

- Clear evaluation of grants, pledges, and contributions can help nonprofits recognize revenue appropriately and support consistent, transparent financial reporting.

- Memberships, sponsorships, and similar arrangements may include both exchange and contribution elements, making thoughtful analysis important for compliance and audit readiness.

How should your nonprofit recognize revenue?

Nonprofit funding continues to grow more complex as funding structures evolve. Pledges, grants, sponsorships, and other arrangements increasingly blend elements of exchange transactions and contributions.

Given this complexity, revisit the fundamentals of distinguishing between exchange revenue and contributions. Understanding this distinction is critical for proper accounting treatment, as well as transparent and consistent financial reporting.

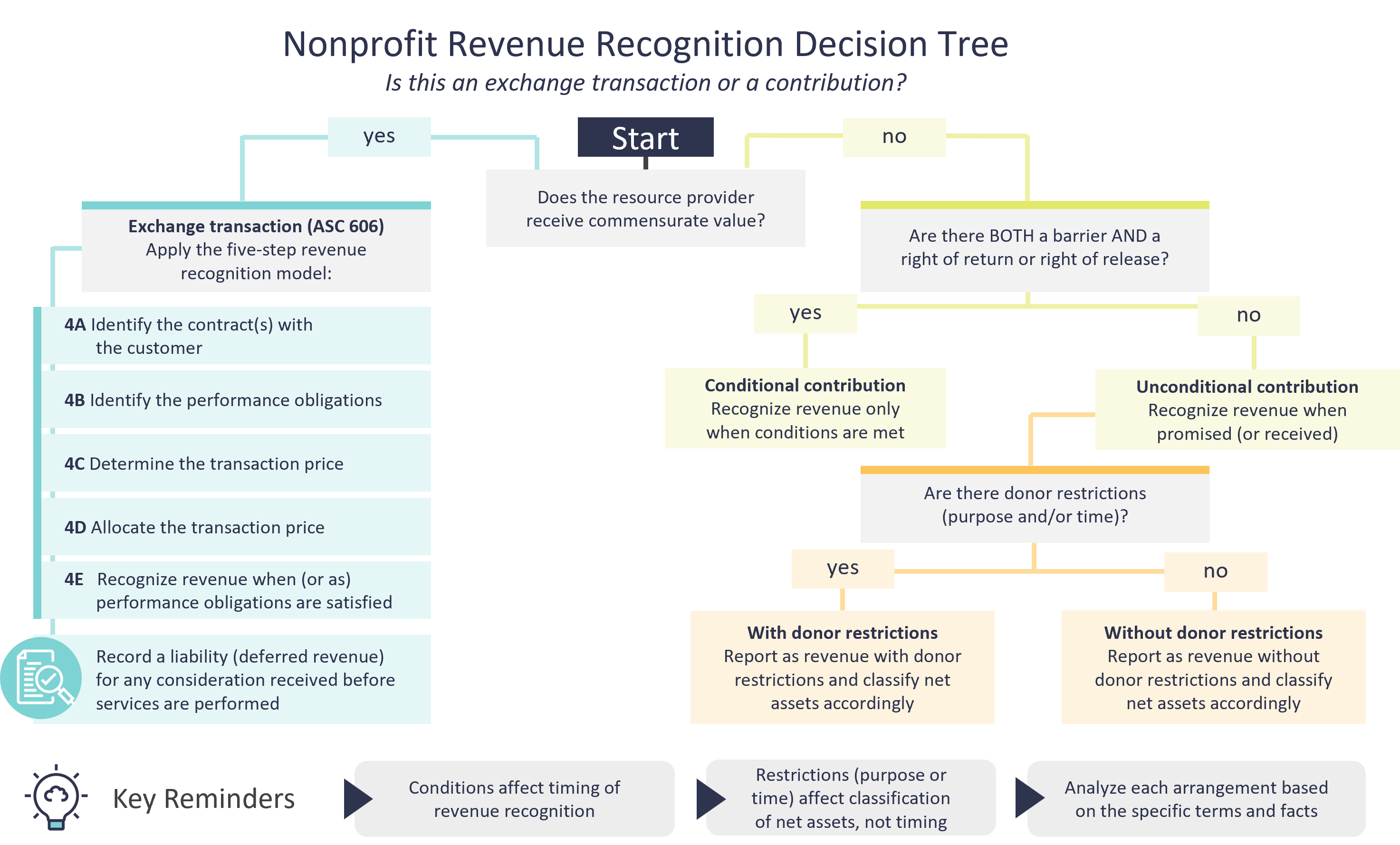

Use the decision tree below to help determine the appropriate accounting model.

1. Determine whether the transaction is an exchange or contribution

Assess whether the resource provider receives commensurate value.

- Exchange transaction (ASC 606) — Both parties receive something of comparable value.

- Contribution (ASC 958) — The transfer is nonreciprocal; the provider doesn’t receive direct value.

A common misconception is government grants are always exchange transactions because they benefit the public. However, unless the resource provider (e.g., government agency) receives direct value, the arrangement is typically a contribution, which may or may not be conditional depending on the terms.

2. If the funding is a contribution, determine whether it’s conditional

Not all contributions are recognized immediately. A contribution is conditional only if both exist:

- A measurable barrier (e.g., performance milestones, matching requirements), and

- A right of return or right of release

If both exist, revenue is recognized only when the condition is met. If not, revenue is recognized when promised or received.

Key reminder: Administrative requirements (e.g., reporting) are generally not considered barriers.

3. Evaluate donor restrictions (separate from conditions)

Conditions determine timing, but restrictions impact classification. Common types of donor restrictions:

- Purpose restrictions (e.g., specific program or project)

- Time restrictions (e.g., funds to be used in future periods)

Contributions can be both conditional and restricted — these are separate analyses.

4. For exchange transactions, apply ASC 606

If a transaction is determined to be an exchange transaction, organizations apply the five-step revenue recognition model under ASC 606. This model involves:

- Identifying the contract

- Determining the performance obligations

- Establishing the transaction price

- Allocating that price to each performance obligation

- Ultimately recognizing revenue as those obligations are satisfied

Revenue recognition rules for memberships, sponsorships, and other special arrangements

When ASC 606 was first introduced, many nonprofits with sponsorship revenue focused heavily on identifying each promised benefit included in membership dues and sponsorship arrangements. This often proved challenging, particularly because many of these benefits aren’t distinct.

In those situations, the benefits should generally be bundled together and treated as a single performance obligation. For example:

Typical membership or sponsorship benefits — such as ongoing access, advocacy or representation, newsletters or publications, and general networking opportunities — are often highly interrelated. As a result, it’s often appropriate to account for them as a combined package of benefits rather than separate deliverables.

Organizations tend to run into challenges when certain goods or services are also sold separately as distinct performance obligations. Common examples include conference registrations, exhibit booths, and specific advertising placements. These items more clearly represent standalone deliverables rather than part of a broader bundle.

As a result, in practice, organizations generally follow one of two approaches:

- Bundled model — Combining multiple related benefits into a single performance obligation

- Hybrid model — Bundling a core set of benefits while separately identifying one or more distinct, event-based or deliverable-specific obligations

Not all elements of a sponsorship arrangement are necessarily exchange transactions. For example, sponsorship may include exchange-based components (such as registrations, exhibits, or advertisements), alongside non-exchange components for general support of the organization’s mission.

This is an area where practice has evolved significantly. In the past, organizations commonly treated sponsorship arrangements entirely as exchange transactions. Increasingly, however, there’s a more thoughtful bifurcation — separating exchange components accounted for under ASC 606 from contribution elements accounted for under contribution guidance.

How CLA can help nonprofits with revenue recognition under ASU 2018-08

Accounting Standards Update (ASU) 2018-08 is the Financial Accounting Standards Board rule for how nonprofits should account for grants and contributions. We can help nonprofits comply with the rule.

- Evaluate grant and contract language

- Design revenue recognition policies

- Identify and correct misstatements

- Improve audit readiness

- Train internal finance teams on ASC 958 and ASC 606

Contact us

Not sure how your nonprofit should recognize revenue? Complete the form below to connect with CLA.