Key insights

- A proposed change to capital rules would affect how community banks measure their regulatory capital ratios.

- Mortgage-related capital treatment may become less restrictive, which could change the economics of servicing and origination for some community banks.

- New loan-to-value tiers and a “cash flow dependent” concept shift the focus to credit risk, underwriting documentation and data quality.

- A simplified conversion factor for certain unused commitments could move RWAs for banks not using CBLR — worth modeling early.

- The comment period is a chance to shape definitions and implementation timing — especially where operational burden could drive inconsistent results across banks.

Need a regulatory capital technical impact assessment?

Regulators are proposing changes that could make some mortgage activity “cost less” in capital terms.

If your bank holds mortgage servicing rights or carries residential mortgages and unused commitments, this proposal could shift your risk‑weighted assets and capital ratios.

The catch: To take advantage of the changes (or even gauge the impact), many banks will need cleaner loan level data than they track today.

The comment period for these proposed changes closes June 18, 2026.

What is the proposed rulemaking on bank capital?

The FDIC, Federal Reserve Board, and Office of the Comptroller of the Currency are requesting comment on a proposal to modernize the regulatory capital framework by revising certain elements of:

- The definition of regulatory capital, and

- The calculation of risk-weighted assets under the standardized approach.

The proposed changes aim to “improve risk sensitivity while generally retaining the simplicity of the current framework.” These proposed modifications to the capital rule, in part, come in response to the comments received from Economic Growth and Regulatory Paperwork Reduction Act (EGRPRA) process.

Why this matters to community banks

If adopted, these changes could:

- Make mortgage lending more practical

- Reduce pressure on capital ratios

- Cut down on rule-driven workarounds

- Lower compliance friction tied to technical details

Regulators issued this proposal alongside a separate request for comment on the expanded risk-based approach. The proposed changes summarized below emphasize the impacts most likely to affect community banks using the standardized approach (“covered banks” — <$100B, not Category I – IV).

The most impactful and favorable changes to regulatory capital framework appear to be aligned with broader policy objectives in the U.S. housing market to alleviate regulatory disincentives placed on banks which serve as the primary intermediary supplying credit to households and nonfinancial firms.

When banks face higher risk-based capital requirements, they typically reduce lending to decrease risk-weighted assets and sometimes transfer higher funding costs to borrowers through increased interest rates, the agencies noted.

Our take:This proposal isn’t just accounting mechanics. It’s an attempt to remove capital “friction” that can quietly steer banks away from certain mortgage activities. Banks that can quantify the change may gain room to rethink origination, servicing, and pricing — especially where regulatory capital limitation has been part of the story.

How the proposal rebalances mortgage risk and capital

The agencies aim to promote mortgage origination and servicing by all banking organizations, including those subject to the community bank leverage ratio framework (CBLR) in a risk-conscious way by:

- Removing the mortgage servicing asset (MSA) deduction from common equity tier 1 (CET1) capital

- Introducing a loan-to-value (LTV)-based approach for assigning risk weights to certain residential mortgage exposures

Agencies aim to modernize capital rules to incentivize community banks to lend and service residential mortgages.

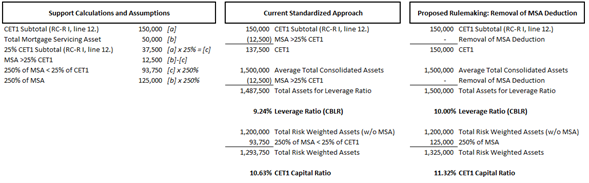

Removal of MSA deduction

The proposed rulemaking revises the definition of regulatory capital by eliminating the requirement to deduct any amount of MSAs from CET1 capital. The current definition requires MSAs exceeding 25% of CET1 capital to be deducted from regulatory capital.

This is favorable treatment for standardized approaches, regardless of CBLR election. The entire carrying amount of the MSA will now be subject to 250% risk weighting, consistent with the component not previously exceeding the 25% CET1 deduction threshold.

Despite that additional amount becoming subject to the 250% risk weighting, the net effect remains favorable as shown in the pro forma illustration below of how a $1.5 billion standardized approach institution would report a $50 million MSA.

To the extent banks don’t have MSAs or MSAs don’t exceed 25% of CET1 capital, this component of the proposed rules will not impact their regulatory capital.

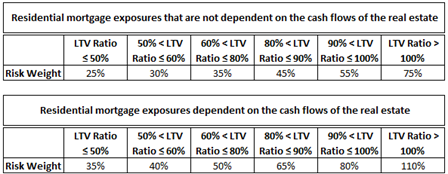

LTV-based approach to risk weighting residential exposures

The proposed LTV-based approach would further differentiate risk weights based on whether a residential mortgage is dependent on cash flows generated by the real estate securing the extension of credit to better align the risk sensitivity of those activities.

The proposal says “Residential mortgage exposures that are dependent on such cash flows to repay the loan can also be more affected by local market conditions and, thus, present elevated credit risk. For example, an increase in the supply of competitive rental property could lower rental prices and suppress cash flows needed to support repayment of the loan.”

If the underwriting process at origination of the residential mortgage exposure considers any cash flows generated by the real estate securing the loan, such as from rental payments, the exposure would be deemed dependent on the cash flows generated by the real estate.

To qualify to use the tiered LTV-based risk weight, the residential mortgage exposure would be required to:

- Be secured by a property that is either owner-occupied or rented

- Be made in accordance with prudent underwriting standards, including relating to the loan amount as a percent of the value of the property

- Not be 90 days or more past due or carried in nonaccrual status

- Not be restructured or modified

Consistent with the current capital rule, residential mortgage exposures that do not meet the above criteria or are a junior lien residential mortgage exposure would continue to receive a 100% risk weight.

To the extent banks elect the CBLR, this component of the proposed rules won’t impact their reported regulatory capital.

What may surprise banks

The biggest lift may not be the math; it’s the data and documentation. If the final rule ties risk weights to LTV and whether underwriting considered rental cash flows, banks will likely want consistent loan level fields (and repeatable decision rules) to support classification across origination channels and acquired portfolios.

Off-balance-sheet credit exposures

Consistent with the objectives of the modernization of the regulatory capital framework, the proposal also aims to:

- Address inconsistent application of the current definition of commitment

- Simplify the conversion factors applied to unused commitments that are not unconditionally cancellable for risk weighting purposes.

Commitments

The proposed rulemaking addresses inconsistent application of the current definition of a commitment by clarifying that a commitment must be a contractual, legally binding obligation for the bank to extend credit, thereby excluding informal arrangements or purely discretionary exposures.

Checklist: What banks can do next:

- Snapshot MSAs and model the capital-ratio effect

- Identify where LTV and cash-flow reliance are tracked (and where they aren’t)

- Flag mortgage products that may be “cash-flow dependent”

- Review unused commitments under the clarified definition

- Decide what feedback to raise during the comment period

For example, “A commitment does not include pre-approval letters for residential mortgage loans, credit card offers, or other offers that have not yet been agreed upon by both parties to the transaction.”

Other detailed examples of various credit arrangements are provided to promote consistent application of the definition of commitment and proper identification between those that are conditionally and unconditionally cancellable.

This expanded definition should be considered by all covered banks as total off-balance sheet exposures noted in RC-R Part I, item 34.a. – 34.c., including unused portions of conditionally cancellable commitments still cannot exceed 25% of consolidated assets to qualify for the CBLR election.

For covered banks that don’t make a CBLR election, the calculation of risk-weighted assets under the standardized approach would change as described below.

Conversion factors

Under current rules, unused commitments that aren’t unconditionally cancellable receive different credit conversion factors based on original maturity:

- 20% for commitments of one year or less

- 50% for those longer than one year

Under the proposal, those same commitments would be subject to a 40% credit conversion factor, regardless of maturity. Modeling the impact on risk-weighted assets should steer comments from community banks as to whether the simplification of the proposed rule outweighs any potential unfavorable impact on risk-weighted assets.

Removing the one-year mark as a dividing line between substantially different treatments would remove any regulatory incentive to structure transactions around that line.

Banks have a window to comment on these proposals; this is the moment to understand how the changes might affect lending strategy, capital planning, and data tracking going forward.

Other technical amendments

On November 12, 2025, FASB issued ASU 2025-08, “Financial Instruments—Credit Losses (Topic 326): Purchased Loans,” which amends the guidance on accounting for purchased loans.

Under prior GAAP, acquired financial assets were classified as either purchased credit-deteriorated (PCD) or non-PCD. PCD assets used the gross-up approach, while non-PCD assets recognized an allowance for credit losses (ACL) through provision for credit losses, often resulting in a perceived double-counting of expected credit losses, as credit adjustments were also included in the fair value of loans acquired.

ASU 2025-08 expands the gross-up approach to include purchased seasoned loans (PSL). PSLs are a newly created category of acquired loans not meeting the definition of PCD. This change reduces complexity and improves comparability by minimizing the subjective distinction between PCD and non-PCD assets but requires the agencies to amend the capital rule identifying which ACLs under ASC 326 would be eligible for inclusion in tier 2 capital.

The proposed treatment modifies the term “adjusted allowance for credit losses” (AACL) to define that ACL on PSLs are excluded from AACL. Conceptually, the agencies only intend to include ACLs charged against earnings or retained earnings in tier 2 capital, which is not the case for ACLs on PCD assets and PSLs at the acquisition date.

Even though post-acquisition increases in ACLs for PSLs would be established through the provision for credit losses, the agencies are proposing to exclude the entire ACL on PSL from AACL due to undue complexity and burden placed on banks to bifurcate acquisition date and post-acquisition ACLs on PSLs.

How CLA can help banks with regulatory changes

CLA works with community banks to translate proposed capital changes into practical decisions. We can help you:

- Quantify the impact on RWAs and capital ratios under the standardized approach, including MSAs and unused commitments

- Create repeatable loan classification rules for LTV tiers and “cash flow dependent” exposures that align with underwriting practice and documentation

- Strengthen loan-level data so the fields needed for reporting and internal modeling are consistent across systems and portfolios

- Support comment-letter development with portfolio evidence, operational considerations, and implementation timing that regulators can act on

Our approach helps banks align capital planning, product strategy, and governance with evolving regulatory expectations while maintaining operational simplicity.

Contact us

Need a regulatory capital technical impact assessment? Complete the form below to connect with CLA.