Financial institutions should complete a regular analysis of their HMDA data not only to prepare for their regulatory exam, but to prepare for public response.

Starting with the 2018 Home Mortgage Disclosure Act (HMDA) data collection, regulators are now able to include more data in their initial analysis. This could help streamline fair lending exams, as the expanded Loan Application Register (LAR) data may help explain any disparities upfront.

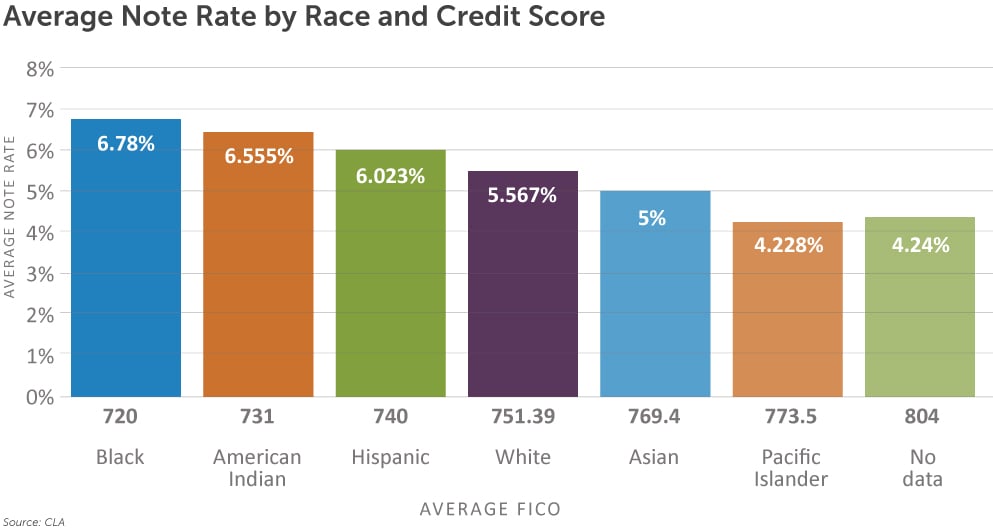

For example, the expanded HMDA LAR data now includes interest rate, loan term, introductory rate period, and credit score. This information may be used to review pricing trends among race and ethnicity groups, with explanation of outliers covered by the additional information already included on the LAR.

Conversely, analysis of the new HMDA data could uncover trends a financial institution may not have been aware of. It is crucial for institutions to be completing a regular analysis of their own HMDA data, not only to prepare for regulatory exam, but also to prepare for public scrutiny.

“Where a lender's underwriting decisions are the subject of a statistical analysis, detailed information must be collected from individual loan files about the applicants' qualifications for credit. Data reported by lenders under the HMDA do not, standing alone, provide sufficient information for such an analysis because they omit important variables, such as credit histories and debt ratios.” - OCC Fair Lending Handbook

Historically, regulators have acknowledged that a statistical HMDA LAR data analysis alone is not enough to establish a pattern or practice of disparate treatment under fair lending standards.

While HMDA data has been a starting point for many a fair lending exam since its inception, the data gleaned from an analysis of the LAR data has been limited to race and ethnicity as prohibited basis factors, and an analysis of mainly disparate high cost status, rate spread, action taken, and location. Where a trend emerged from the data analysis, the regulator would then schedule a deeper review into a financial institution’s fair lending practices, requiring the institution to provide further documentation and the option to include an explanation. At loan level, the common exonerating factors would often be the underwriting criteria utilized, such as credit score, to explain the appearance of a pricing disparity.

What story will your 2018 HMDA data tell?

Approval and denial rates are typically not used alone to determine disparities. The Interagency Fair Lending Examination Procedures state, “Gross HMDA denial or approval rate disparities are not appropriate for disproportionate adverse impact analysis because they typically cannot be attributed to a specific policy or criterion.”

However, the expanded 2018 HMDA data allows for approval and denial rates to be filtered by other relevant data to form an initial analysis: Debt to income ratio, credit score, and other factors may be utilized.

The Interagency Procedures provide an outline of residential lending discrimination risk factors, only two of which refer to HMDA data specifically in the areas of pricing and redlining:

P6. *In mortgage pricing, disparities in the incidence or rate spreads of higher-priced lending by prohibited basis characteristics as reported in the HMDA data.

R1. *Significant differences, as revealed in HMDA data, in the number of applications received, withdrawn, approved, not accepted, and closed for incompleteness or loans originated in those areas in the institution's market that have relatively high concentrations of minority group residents compared with areas with relatively low concentrations of minority residents.

Other risk factors that may be informed by pre-2018 HMDA data in the underwriting category are:

U2. *Substantial disparities among the application processing times for applicants by monitored prohibited basis characteristic (especially within denial reason groups).

U3. *Substantially higher proportion of withdrawn/incomplete applications from prohibited basis group applicants than from other applicants.

Due to the increase of the data reported on the LAR post-2018, other risk factors identified in the Interagency Procedures are also able to make good use of HMDA data as a starting point, such as those identified in the underwriting category:

U1. *Substantial disparities among the approval/denial rates for applicants by monitored prohibited basis characteristic (especially within income categories).

U7. Relatively high percentages of either exceptions to underwriting criteria or overrides of credit score cutoffs.

Risk factors identified in the pricing and steering categories include:

P4. *Substantial disparities among prices being quoted or charged to applicants who differ as to their monitored prohibited basis characteristics.

P7. *A loan program that contains only borrowers from a prohibited basis group, or has significant differences in the percentages of prohibited basis groups, especially in the absence of a Special Purpose Credit Program under ECOA.

S4. *Significant differences in the percentage of prohibited basis applicants in loan products or products with specific features relative to control group applicants. Special attention should be given to products and features that have potentially negative consequences for applicants (i.e., non-traditional mortgages, prepayment penalties, lack of escrow requirements, or credit life insurance).

All of these risk factors identified may also be further filtered by property location to inform redlining trends when used in conjunction with census tract data that identifies areas that have relatively high or low concentrations of minority residents.

New data fields use to inform fair lending

Of the newly reportable HMDA data fields, many may be utilized to inform fair lending risk areas.

Underwriting:

- Credit score

- Debt to income ratio

- Combined loan to value

Terms of the loan:

- Total loan costs (including origination charges, discount points, and lender credits)

- Interest rate

- Prepayment penalty term

- Loan term

- Introductory rate period

- Non-amortizing features (balloon, interest only, negative amortization, or other)

- Open-end line of credit or reverse mortgage

Property information (including location and census tract):

- Property value

- Total units

- Total affordable units

- Manufactured home status

All of this information can be sorted by the prohibited basis groups reported on the LAR: race, ethnicity, gender, and applicant age.

The Equal Credit Opportunity Act prohibits discrimination based on the following:

- Race or color

- Religion

- National origin

- Sex

- Marital status

- Age

- Receipt of income derived from any public assistance program

- The applicant’s exercise of any right under the Consumer Credit Protection Act

Expanded HMDA LAR data available to the public

HMDA LAR data will be made available to the public in modified form. Historically, the public data has been used for Fair Housing Act scrutiny — this will not change; however, the expanded LAR data will result in more information available on which to base inquiry. To be competitive, any institution would be wise to use the publically-available data to compare their loan terms against those of their peers in their Reasonable Expected Market Area.

The modified public data will now include:

- Total loan costs, origination, points, credits, interest rate

- Identification of “risky features” such as non-amortizing features, adjustable rates, and prepayment penalties

- Retail versus wholesale origination

The value of the below fields will be disclosed as ranges, rather than exact numbers:

- Loan amount

- Age range

- Debt to income ratio under 36 or over 50 as range

- Property value

- Dwelling units (and income-restricted units)

Public data will NOT include:

- Credit score

- Automated underwriting system result

- Property address

- Originator Nationwide Mortgage Licensing System and Registry identifier

- Most freeform text fields

- Reasons for denial

- Application date and action date

Regulation C examination

The purpose of HMDA data collection is fair lending; however, institutions may also be examined for compliance with the Regulation C reporting requirements. Enforcement actions under Regulation C generally arise due to inaccurate reporting and could result in a resubmission requirement or civil money penalties.

Inaccurate HMDA reporting uncovered during a Regulation C examination could result in the beginning of a fair lending examination. The OCC advises in their fair lending handbook, “[A] person who intentionally submits incorrect or incomplete HMDA data in order to cover up a violation of the Fair Housing Act may be subject, under the Fair Housing Act and federal criminal statutes, to a fine or prison term or both. In addition, a failure to ensure accurate HMDA data may be considered as a relevant fact during a Fair Housing Act investigation or an examination of the institution's lending activities.”

How we can help

Ensuring your HMDA data is accurate and properly recorded and your LAR is submitted on time are the first steps to a reliable fair lending analysis.

CLA Mortgage Advisory Services provides mortgage lenders with HMDA LAR data integrity checks and data analysis reporting. Our mortgage advisory team can help you navigate mortgage compliance, quality control, and fair lending as you work to uncover your HMDA data story.