Key insights

- Tax credit transferability under the Inflation Reduction Act has created an alternative to tax equity investments in renewable energy projects.

- Strong motivations remain for renewable energy developers and certain companies to pursue tax equity investments.

- For companies looking for tax savings without a long-term commitment to a project sponsor, transferability is a powerful planning tool to explore.

Find out if tax credit transferability can increase your savings.

Tax credit transferability under the Inflation Reduction Act of 2022 (IRA) has changed the landscape for monetizing federal clean energy credits. Historically, extracting investment and production tax credits for a renewable energy project has required a tax equity investment, committing an investor to a project (typically for multiple years) through a variety of potential ownership structures the IRS allows.

The IRA creates an attractive alternative to tax equity by allowing these credits to be bought and sold for cash. Companies hungry for tax savings may now choose to tap into a burgeoning tax credit marketplace rather than work with a sponsor to fund a long-term renewables deal.

The Inflation Reduction Act is a game changer for investing in clean energy, offering new tax incentives and financing opportunities. Learn how you can benefit.Visit our IRA Resource Center

While strong motivations remain for developers and certain investors to pursue tax equity investments, transferability adds some optionality for investors to analyze when evaluating tax goals.

Tax equity at a glance

The U.S. tax code — and more recently the IRA — provides incentives for companies to invest in certain areas, specifically renewable energy. Renewable energy project developers are typically unable to use these tax benefits themselves, thus a “tax equity” market developed to attract capital from corporate taxpayers to assist in funding projects. There are several key terms to understand and consider in a traditional tax equity structure:

- Sponsor — Developer who lacks sufficient tax base to monetize tax credit and depreciation benefits

- Investor — Cash taxpayer who uses available cash to generate a targeted return on investment (ROI) or internal rate of return (IRR) from allocated tax benefits

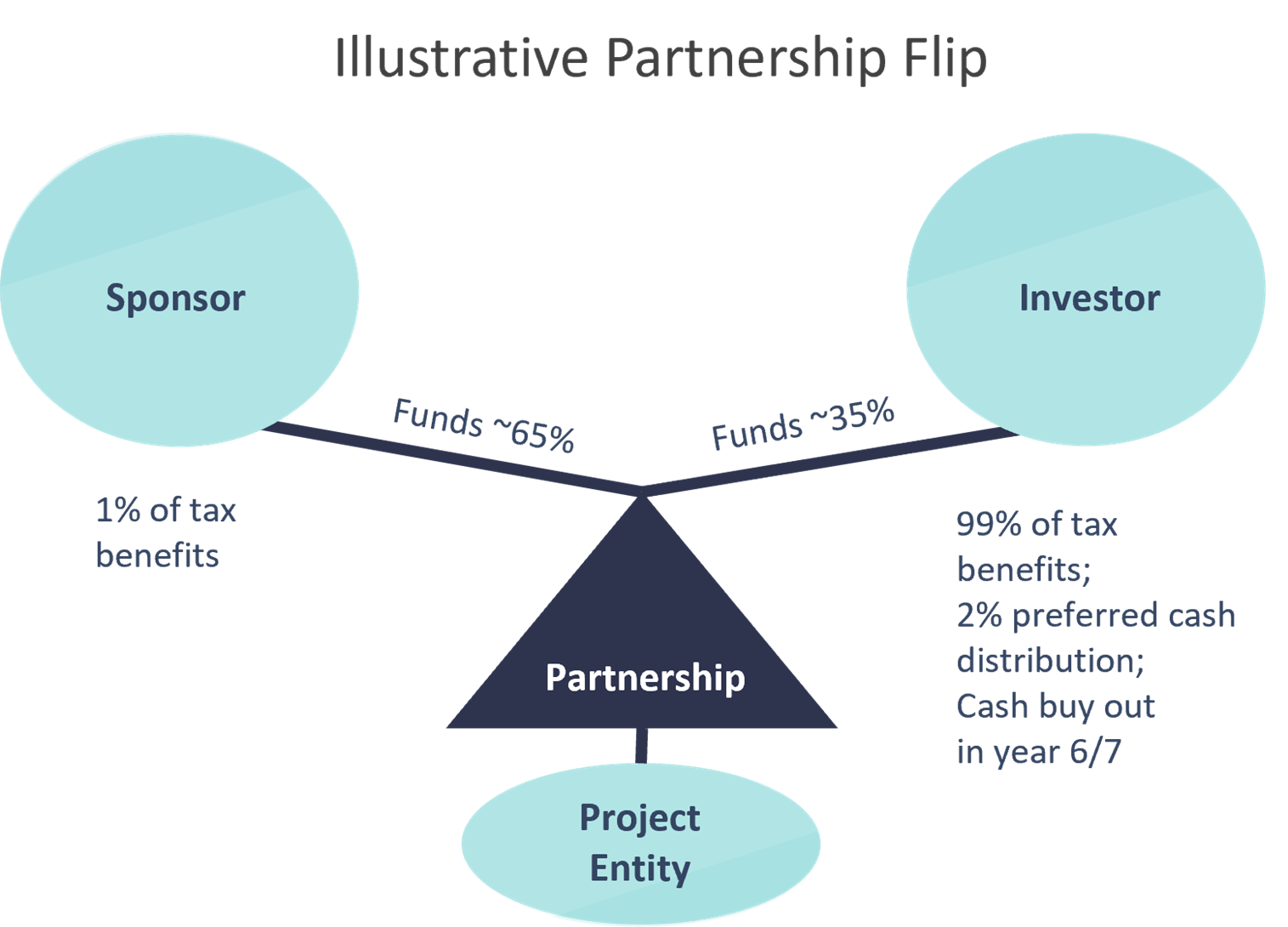

While there are several types of tax equity structures (i.e., partnership flips, sale leasebacks, and inverted leases), the partnership flip structure is commonly used — given it’s relatively straight forward and widely known in the industry.

For investors, the cash outflow is the upfront cash (i.e., tax equity) investment. The expected cash inflows include (1) reduced cash tax liability via receipt of tax credits and accelerated tax depreciation, (2) quarterly or annual preferred cash distributions, and (3) end of deal cash buy-out.

In a typical partnership flip transaction, the partnership allocates 99% of income, loss, and tax credits to the investor until it reaches a target yield (cash is shared in a different ratio). After the yield is reached, the investor’s share of benefits decreases, and the developer may buy the investor’s remaining interest (which is typically exercised). See below for an illustrative partnership flip structure:

Transferabilty under the IRA

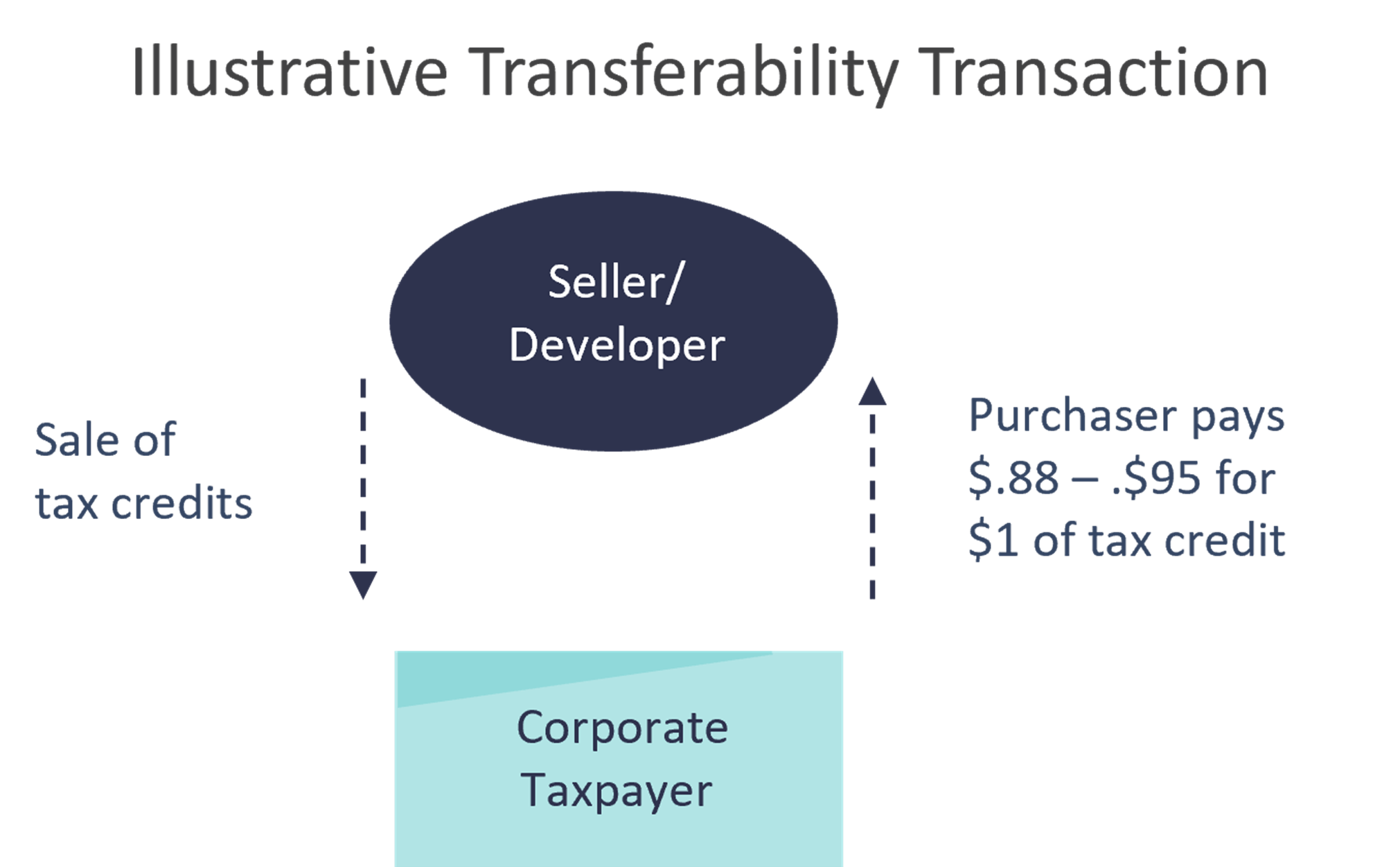

The IRA permits tax credit transfers (i.e., sales) of 11 tax credits previously unavailable under U.S. federal income tax law. Any “eligible taxpayer” may sell tax credits, which generally includes for-profit corporations (including S corporations), partnerships, individuals, and trusts. Entities eligible to use the elective pay election for direct cash refunds such as tax-exempt organizations and local governments are not eligible to transfer credits. While the tax credit transferability landscape is still evolving, the current marketplace facilitates purchasing discounted credits with a shortened investment period and streamlined legal process as compared to some traditional tax equity investments.

The tax credit purchase price can vary based on the seller’s creditworthiness, project size, credit type and amount, and existence of tax insurance. Credit purchases must be made in cash by an unrelated party and can only be sold once. The credit is transferred by means of a legal purchase and sale agreement and a transfer election statement is attached to the seller’s and purchaser’s tax return for the applicable tax year. On December 22, 2023, the IRS released an online registration system where the seller must register for and receive a registration number for any transferred credits. See below for an illustrative tax credit transferability transaction:

Which strategy to pursue

There should continue to be a robust market for both traditional tax equity and tax credit transferability transactions. Developers will likely remain incentivized to pursue tax equity investments to monetize tax depreciation benefits that are not included in tax credit transfer scenarios. Tax equity investors are analyzing opportunities where they participate in a traditional tax equity structure and subsequently transfer the credits in a separate transaction.

In either tax equity or transferability transactions, the investor should pursue due diligence procedures and tax insurance to limit risk. The seemingly more straightforward tax credit transferability transactions are already attracting many new investors into the sector. Ultimately, each developer and investor will make an independent determination whether tax equity, transferability, or both make the most sense for their specific situation.

How we can help

CLA’s energy services team can help you evaluate strategies to meet your clean energy and tax-saving objectives. From cash flow modeling to tax credit consulting and compliance, our team focuses on end-to-end planning for renewable energy project investors and developers.

Contact your CLA professional to learn how we can help your organization comply with these new rules.