Technology giants continue to lift the broad U.S. equity market, bonds stay on the up side, and the Fed makes another move on interest rates.

As we look back on the second quarter of 2017, the news and market data are mostly positive. One of the brightest spots is the technology sector, which is boosting overall market performance. We’ll take a close look at the forces behind this trend and its impact on other parts of the domestic and global economy. But first, a side-by-side of the positive and negative signs in the broader economy.

| Positives | Negatives |

|---|---|

|

|

Second Quarter and Year-to-Date 2017 Index Returns (%)

| Index Name | Capital Market Segment | 2Q 2017 | 2017 YTD |

|---|---|---|---|

| Barclays U.S. Aggregate | U.S. Broad Market Bonds | 1.5 | 2.3 |

| S&P 500 | U.S. Large Cap | 3.1 | 9.3 |

| Russell 2000 | U.S. Small Cap | 2.5 | 5 |

| MSCI EAFE | Non-U.S. Developed Markets | 6.1 | 13.8 |

| MSCI EM | Emerging Markets | 6.3 | 18.4 |

| Hypothetical 60/40 Portfolio1 | Diversified Mix of Indexes | 3 | 7.4 |

140% Barclays U.S. Aggregate, 32% S&P 500, 7% Russell 2000, 16% EAFE, and 5% EM

An investor cannot invest directly in an index, and the hypothetical portfolio is not intended to reflect any specific portfolio managed by CLA Wealth Advisors. An unmanaged index does not reflect any expenses that may be associated with an actual portfolio.

Source: Morningstar

Energy sector slumps as broad markets gain

Asset prices continued to rise against a backdrop of mostly positive economic news. Corporate earnings are robust, with nine of the 11 sectors tracked by the S&P 500 on track to post earnings growth for the second quarter of 2017 (FactSet, June 23, 2017). The U.S. housing market remains firm, with May seeing existing home sales rise and the average sale price up nearly 6 percent from a year earlier (National Association of Realtors).

Large company stocks, boosted by big gains in the technology sector, posted a 3.1 percent gain for the quarter and are up more than 9 percent on a year-to-date basis (S&P 500 returns). Small company stocks posted a modest gain for the quarter and stand at 5 percent year to date. Stock price volatility continues to relatively low; the Chicago Board Options Exchange Volatility Index (VIX), as of the end of May, trades at a 25-year low (Bloomberg).

The trend of growth-style stocks beating value continued in the second quarter. Investors’ appetite for tech stocks, which typically fall in the growth company category, is reflected in the wide performance gap between these two investment styles so far in 2017. At quarter end, the Russell 1000 Growth Index has returned 15 percent while the Russell 1000 Value Index is up only 5 percent.

The energy sector is one of the very few areas of the stock market experiencing distress. Naturally, the price of crude oil has a major impact on this sector. West Texas Intermediate (WTI) began the year trading at $55 per barrel, fell to a low of $40 per barrel in June before staging a rally just before the end of the quarter (NY Mercantile Exchange). Oil price volatility has hurt the energy patch of the stock market. The S&P Energy Select Sector Index has returned -12.7 percent this year. The prices of bonds issued by energy companies are under pressure as well, and in some cases, “under pressure” is an understatement. One specific example: Bloomberg reports that in February, EP Energy, an oil/gas exploration and production company, issued $1 billion worth of bonds at 100 cents on the dollar. Just a few months later, on June 21, the bonds were trading at 70 cents on the dollar. We’re seeing once again that what’s good for consumers isn’t always good for the energy sector as a whole.

Fed rate rises as bonds stay positive

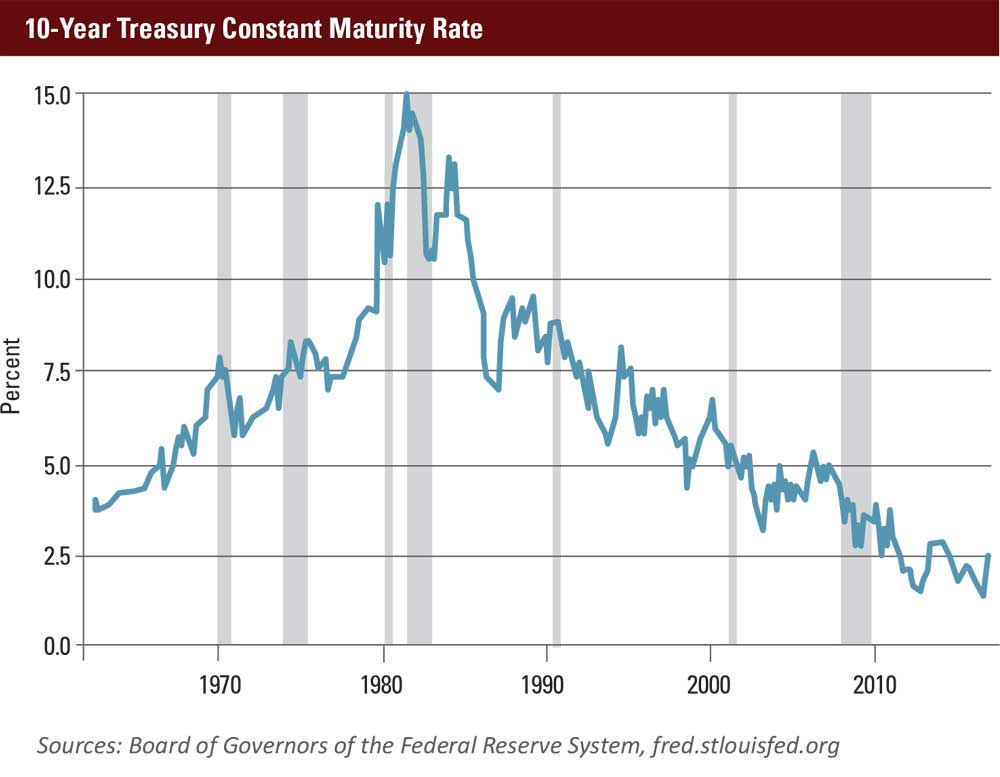

The U.S. bond market provided positive returns for the quarter. The widely-followed Bloomberg Barclays U.S. Aggregate Index has a year-to-date total return of 2.3 percent, which happens to match the year-ending yield on the bellwether 10-Year U.S. Treasury note. The Federal Reserve, as expected, provided a rate increase of one quarter of 1 percent (or 25 basis points, in investment industry terms). The Fed’s comments on the economy were quite sanguine, as they cited improving employment data, robust consumer spending, and a generally strong business environment. Most analysts expect one more rate increase of 25 basis points later this year.

The tax-exempt portion of the fixed income markets also has upward momentum. The Bloomberg Barclays Municipal Index was up 2 percent for the quarter and stands at 3.6 percent year to date. However, there is one notable exception to the general municipal bond market momentum. The state of Illinois is undergoing severe fiscal distress that’s negatively affecting its bonds. The Illinois legislature failed to pass a budget for two years, leaving the state with $14.5 billion in unpaid bills and $800 million in interest and late fees. It is already the lowest-rated state, and the credit ratings companies have warned of further downgrades. If that happens, the nation’s fifth most populous state would become the first to have its general obligation debt rated as “junk” (i.e., below investment grade). Lawmakers finally approved an annual spending plan and tax increase in the first week of July by overriding the governor’s veto, but the Land of Lincoln is still in dire financial straits. Despite this pocket of distress, the broad municipal market is stable and should benefit from the positive macroeconomic backdrop of increasing property values and low unemployment.

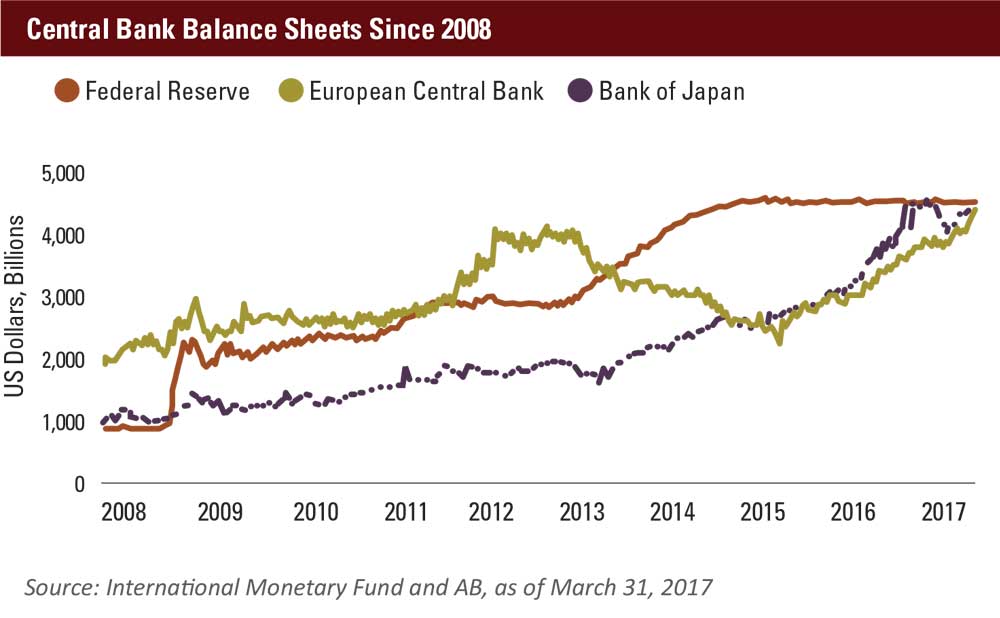

In addition, the Fed has been discussing reducing its $4.5 trillion balance sheet. Such massive numbers are difficult to comprehend, but we can use increments of time as an analogy to put the daunting scale into perspective.

- There are 1 million seconds in 11 days

- 1 billion seconds ago it was 1985

- 1 trillion seconds ago it was 29,693 B.C., or 31,710 years ago

It is an open question as to whether the Fed can successfully unwind its balance sheet and return to a “normalized” interest rate environment. There is no precedent for the extraordinary monetary interventions the U.S. central bank has undertaken since the financial crisis. It’s also important to remember that the Fed is not the only central bank that has pursued such policies. The European Central Bank and the Bank of Japan also have balance sheets topping $4 trillion.

Strong international and emerging markets

In the fourth quarter 2016 issue of Market and Economic Outlook, we emphasized that international and emerging markets, despite having underperformed the U.S. markets by a wide margin over the previous seven years, remained key components of a well-diversified equity portfolio. This was in no way a prediction of what was to come this year, but diversified investors will be gratified to see their non-U.S. holdings adding value in 2017. Developed market stocks, as measured by the MSCI EAFE index, posted a 7 percent return for the second quarter of 2017 and are up 13.8 percent for the year. Key European markets such as France and Germany, are up about 13 percent year to date.

In the first quarter of 2017 issue of Market and Economic Outlook, we wrote about positive sentiment in the United States. A May 2017 survey of German business confidence posted its highest reading in more 25 years ― a good sign for Europe’s largest economy (Ifo Institute, Bloomberg). The capital markets also responded favorably to the recent presidential election in France, in which the populist candidate was defeated. Meanwhile, the United Kingdom is in the midst of some political turmoil and much uncertainty regarding its exit from the European Union (Brexit), but the main stock index has posted a gain of 10 percent in U.S. dollar terms.

The stock markets of the developing world are soaring. The MSCI Emerging Markets Index is up 18 percent year to date. However, there is some notable divergence among the biggest markets in the index. China up 15 percent and India up 20 percent, but Brazil, dealing with yet another major political corruption scandal, is down 20 percent so far in 2017. Russia, whose markets and economy are very sensitive to oil prices, is down 16 percent (Morningstar country indexes).

China, the world’s second largest economy, had some big news during the second quarter. The index provider, MSCI, granted approval for the inclusion of several hundred Chinese large cap stocks that trade on the Shanghai exchange (known as “A” shares). For several years running MSCI rejected inclusion of these stocks based on several concerns, including lack of transparency and availability to non-Chinese investors. The inclusion of these Shanghai-listed stocks is seen as a victory for Chinese government and will also have material impacts on the Chinese market and the MSCI Emerging Markets Index. Reuters reports that Chinese stocks could see an inflow of $400 billion in the next 10 years from asset managers, pensions, and other investors who track the MSCI Emerging Markets Index.

Dollar trending downward against foreign currencies

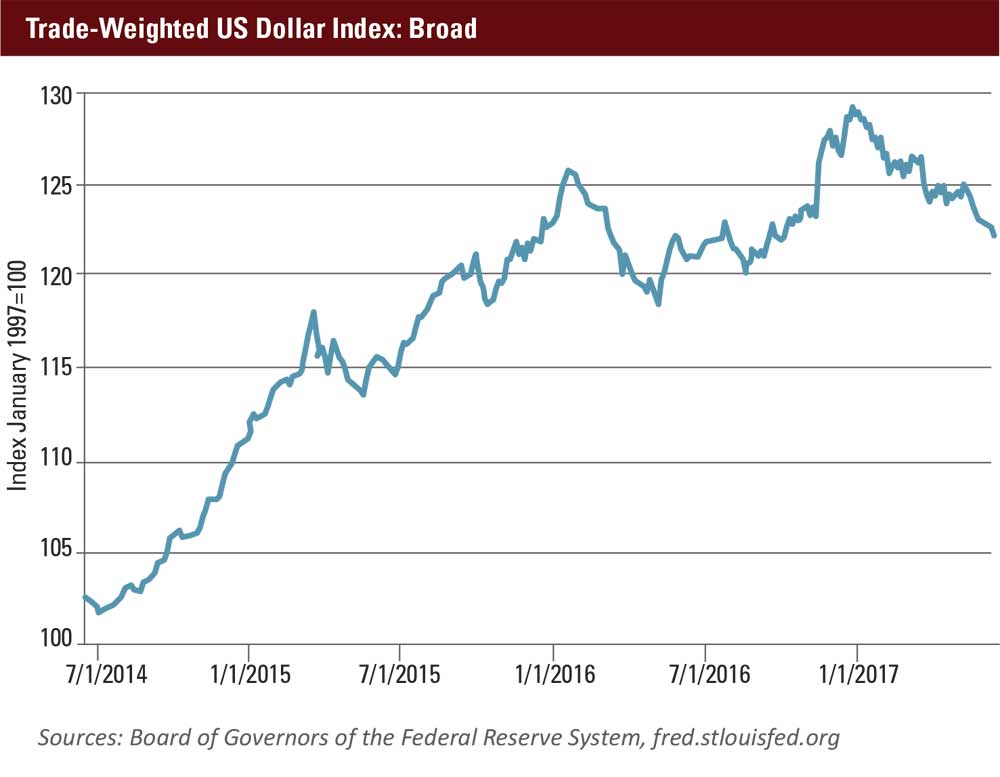

The relative strength of the U.S. dollar (USD) has innumerable impacts on the global economy. One important way it impacts nearly all U.S. investors is how changes in the USD versus foreign currencies affect returns of non-U.S. investments. When the dollar is rising, U.S. investors’ returns in international stock holdings will likely be lower.

To help understand why, assume a U.S. mutual fund buys $1,000 worth of a stock listed in London on the Financial Times Stock Exchange (FTSE, which is commonly pronounced “footsie”). It executes the transaction in British pounds sterling, not U.S. dollars. Let’s assume the stock’s price remains unchanged on the FTSE, but the dollar strengthens by 5 percent against the pound. The stock would be worth the same amount in pounds but now would be worth just $950, and marked as such by the U.S. mutual fund, reflecting a realized loss. Over the last three years for the period ending May 31, 2017, the strength of the dollar has detracted more than 5 percent per annum on average (based on MSCI All Country World Index excluding USA, Hedged Versus Unhedged Indices; Morningstar).

The corollary is this: A weakening dollar augments international returns. In 2017, the U.S. dollar has been trending down, providing a tailwind to international and emerging market holdings this year.

FAANG stocks drive broader markets higher

The investment industry loves a good acronym. In 2015, FANG appeared as shorthand for the names of large cap technology companies that were posting outsized gains and garnering endless financial media attention: Facebook, Amazon, Netflix, and Google. While the S&P 500, a broad U.S. stock index, was up only 1 percent in 2015, the four FANG stocks averaged an 83 percent return between them.

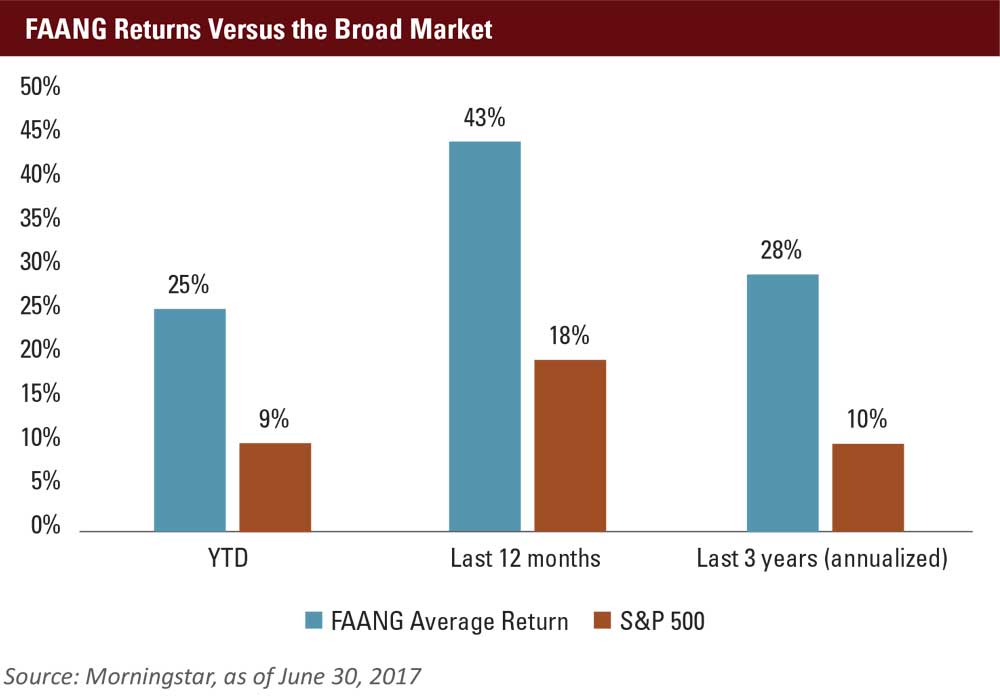

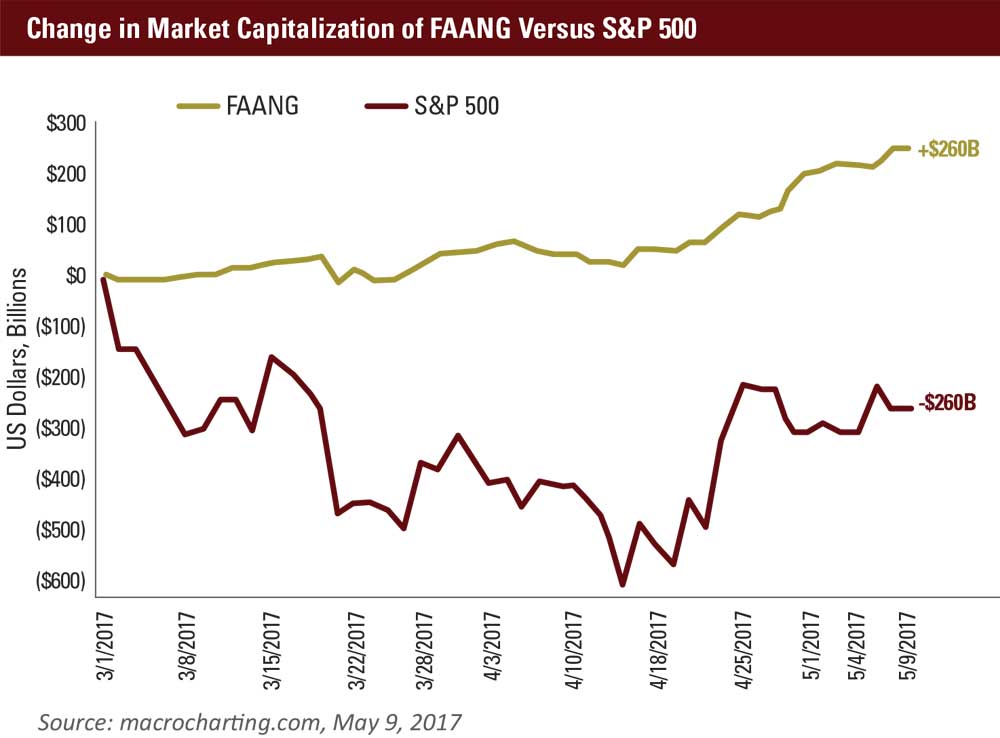

2017 has seen the return of FANG ― or more accurately, FAANG; a vowel was added to accommodate Apple, another hot technology/consumer stock. The degree to which the FAANG stocks have led the broad market is rather remarkable.

Another way to illustrate the strength of FAANG is seen below. For the period of March 31 to May 9, 2017, these five stocks represented 99 percent of the S&P 500’s increase in market capitalization.

Such narrow leadership (meaning that a relatively small handful of stocks or a single sector accounts for most of the broad market’s gains) is generally not viewed as healthy for the market. The FAANG phenomenon, and the underperformance that has resulted from being under-allocated to technology, has left many portfolio managers gnashing their teeth; fewer than one in five actively managed large growth mutual funds have beaten the Russell Growth Index over the last three years (Morningstar, May 31, 2017).

Tech growth ripples through the economy

Some point to the vertical-trending price charts, media attention, and the valuation ratios of technology stocks and see signs of a speculative bubble due to burst at any moment. Others argue that the current prices are justified by high expected earnings growth from these dominant, innovative companies.

Amazon is both an amazing success story and a paragon of investors’ appetite to own shares despite what appear to be sky-high valuations. The company that began as a bookseller is now an on-line retail juggernaut. It also runs Amazon Web Services, selling cloud computing power and technical infrastructure to businesses. Amazon has grown tremendously in recent years, and the price of its shares reflect optimism that that growth will continue. A comparison of Amazon to Walmart tells a story of the market’s current view on old-school brick-and-mortar retailing versus the technology-driven innovator.

| Online Versus Brick and Mortar* | |||||

|---|---|---|---|---|---|

| Company | Total Value of Outstanding Stock (Market Cap) | Revenue Last 12 Months | Net Income Last 12 Months | Current Price-to-Earnings Ratio | Growth in Percent of Earnings Per Share Last 12 Months |

| Amazon (AMZN) | $480 billion | $143 billion | $2.6 billion | 189 | 292 |

| Walmart (WMT) | $226 billion | $488 billion | $13.6 billion | 17 | -4 |

| S&P 500 Average | 21 | ||||

Regardless of your stance on whether Amazon’s stock price is justified by its future growth prospects, it’s undeniable that online retailing is an example of new technologies disrupting entire industries and having wide-reaching impacts on society.

The effect on the jobs market is just one example. The retail industry employs more workers than manufacturing ― about 11 percent of the American non-farm work force (Bureau of Labor Statistics). Many of these jobs are in danger. A report from Credit Suisse estimates that more than 7,000 retail stores will close this year, a higher rate than the number shuttered during the financial crisis of 2008. Thirty percent of commercial real estate is retail, so shuttering stores will also affect that important market.

“Retail technology is driving significant disruption in an industry primarily based on changes in consumer demands and preferences,” says Jeff Sellner, principal and leader of CLA’s technology and emerging industries group. In a relatively short timespan we’ve seen the online shopping experience evolve from just being able to purchase certain consumer products online, to playing a significant role in categories such as clothing, food, and other consumer staples.

“This trend will continue to accelerate,” Sellner adds. “In just a few years the majority of households will buy more goods online than they do in a brick and mortar retail store. Today’s online consumer experience is making it safe and easy to make purchases from your tablet or mobile device and that will require markets that currently rely upon a physical location to innovate their business model to an online consumer experience. Just as an example, consumers may prefer to purchase automobiles completely online rather than spend several hours waiting at a dealership to complete paperwork.”

Sellner also sees technology continuing to infiltrate industries such as manufacturing and trucking where organic growth has become difficult and competition is fierce. “We are seeing many companies invest in technology and software to augment the sales and customer service experience and to find ways to reduce costs through efficiencies. When their needs are not met through commercially available technology, many of these companies that are not traditional technology companies are investing in the development of software tools in house,” Sellner says.

Looking at new technologies more broadly, there are reasons for concern, including job losses, privacy intrusions, and the general existential threat that artificial intelligence (AI) may pose. Indeed, visionaries like physicist Stephen Hawking and entrepreneur Elon Musk have warned that not proceeding thoughtfully with AI could be catastrophic for humankind. We are at the early stages of exciting developments in the fields of AI, virtual and augmented reality, the internet of things, blockchain technology, and many others. Our ability to connect with others, acquire information and knowledge, and pursue individual happiness continues to improve because of technological innovation. The positive effects of technological advancements have been, and will continue to be, a force for positive change in the human condition.

Let the second half of 2017 begin

As we close the book on the first half of 2017, global capital markets continue their stretch of positive returns and modest volatility. That steady course is certainly welcome. We’re now looking with optimism to the second half of 2017, but as always, mindful of the potential risks.