Key insights

- Nearly all sectors of health care services saw increased deal volumes in 2021, spurred by innovations across the industry.

- Investors were encouraged by the ways physician practices used technology to adapt to pandemic-related closures.

- The industry’s heightened capacity to provide at-home care has not discouraged investment in long-term care facilities.

- The pandemic accelerated the shift toward home care and community-based alternatives, and high levels of available capital are fueling deal growth in this segment.

- Increased access to behavioral health care can be attractive to private equity investors and strategic buyers.

Dig into health care deal-making data to help reinforce your transaction decisions.

Recent years have seen a surge of innovation in health care, driven by investments from private equity firms, family offices, and other sources. This elevated interest — particularly in fragmented specialties, home-based care, and behavioral health — is creating growth opportunities throughout the health care sector.

Transaction trends are indicating growth

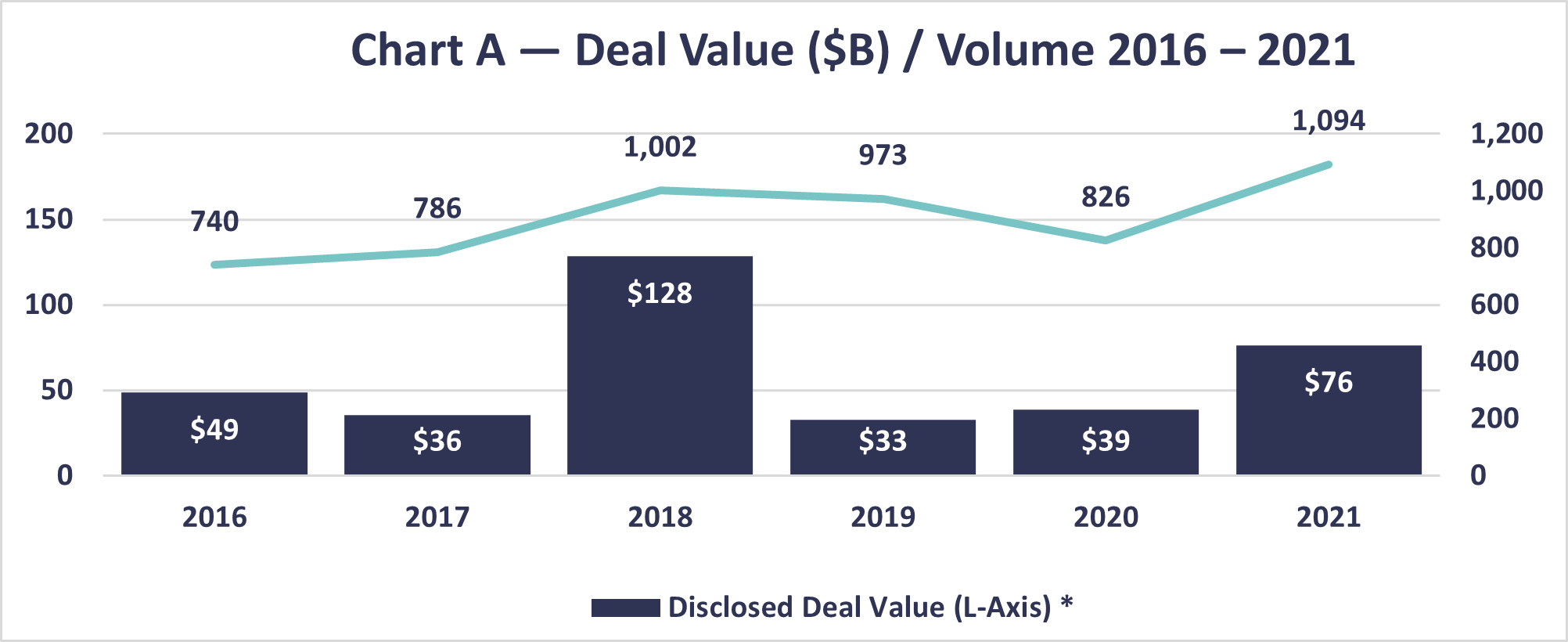

The health care services market showed its resiliency in 2021 — despite no shortage of unknowns resulting from COVID-19. The momentum in deal making from the fall of 2020 carried throughout 2021, with nearly all sectors of health care services seeing increased deal volumes.

Chart A reflects that trend, with more than 250 additional announced transactions in 2021 versus 2020, and more than 100 additional announced transactions in 2021 over 2019. Chart A comprises health care providers including long-term care, physician medical groups, home health and hospice providers, behavioral health care providers, labs, rehabilitation, hospitals, and managed care.

The anticipated capital gains tax changes in 2021 accelerated sellers’ motivation to transact — and headwinds of the ongoing pandemic, economic uncertainty, labor shortages, and high valuation multiples don’t appear to be slowing deal volumes any time soon.

Confidence from financial buyers appears to remain in the health care services sector. Some central themes are:

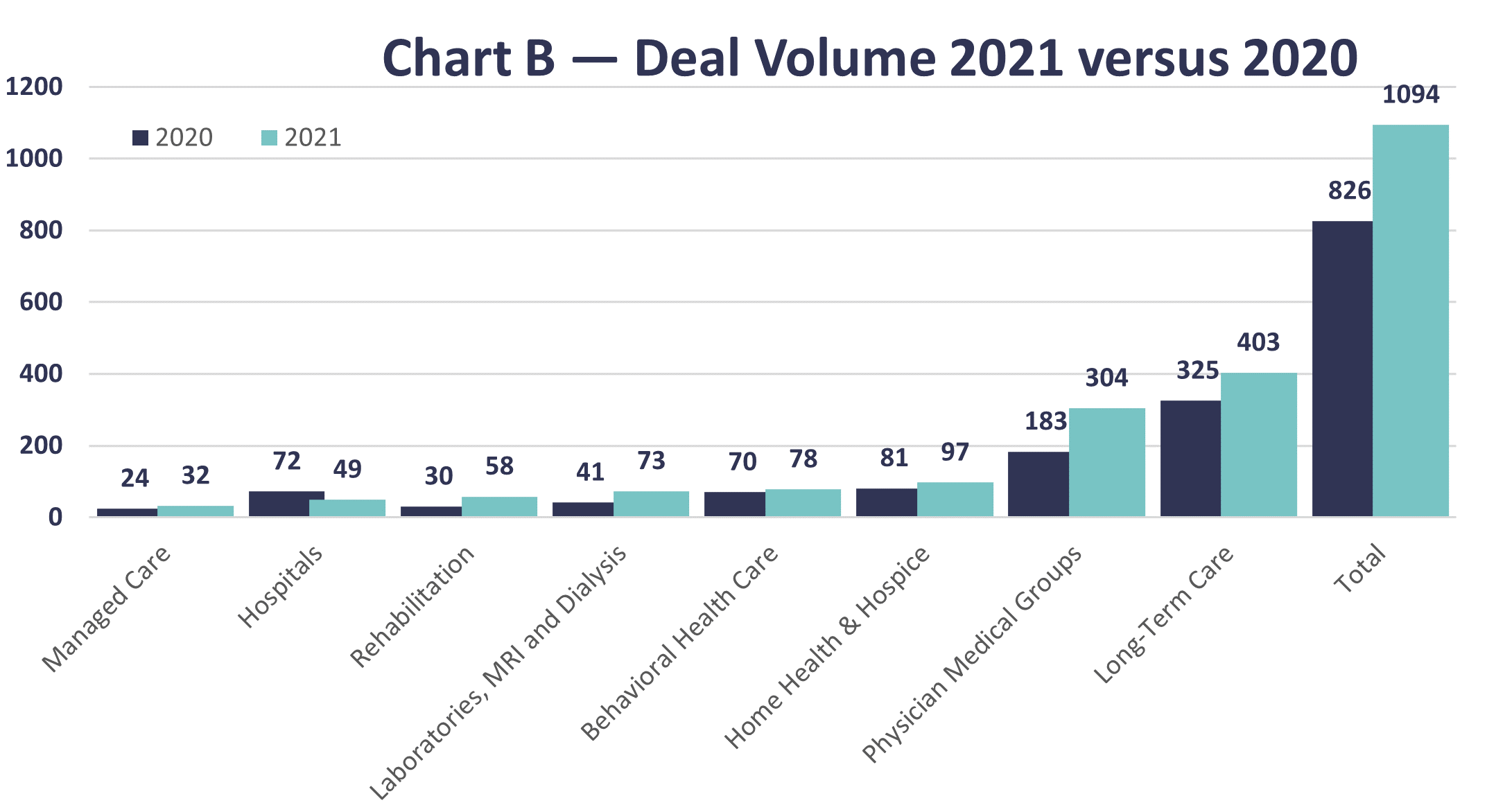

- Private buyers reflecting private equity and strategic buyers are driving the M&A environment due in part to record levels of capital raised, representing nearly 80% of the buying market.

- As shown in chart B, long-term care continues to be the highest segment in terms of volume, followed by physician practices, home health and hospice, and behavioral health providers.

- Geographically, the distribution of deals has a high concentration throughout the Sun Belt region and California.

M&A activity differs among health care segments

Transaction activity seems to be impacted by nuances in the type of health care provider. Let’s explore the M&A activity and outlook of the most transacted health care services segments.

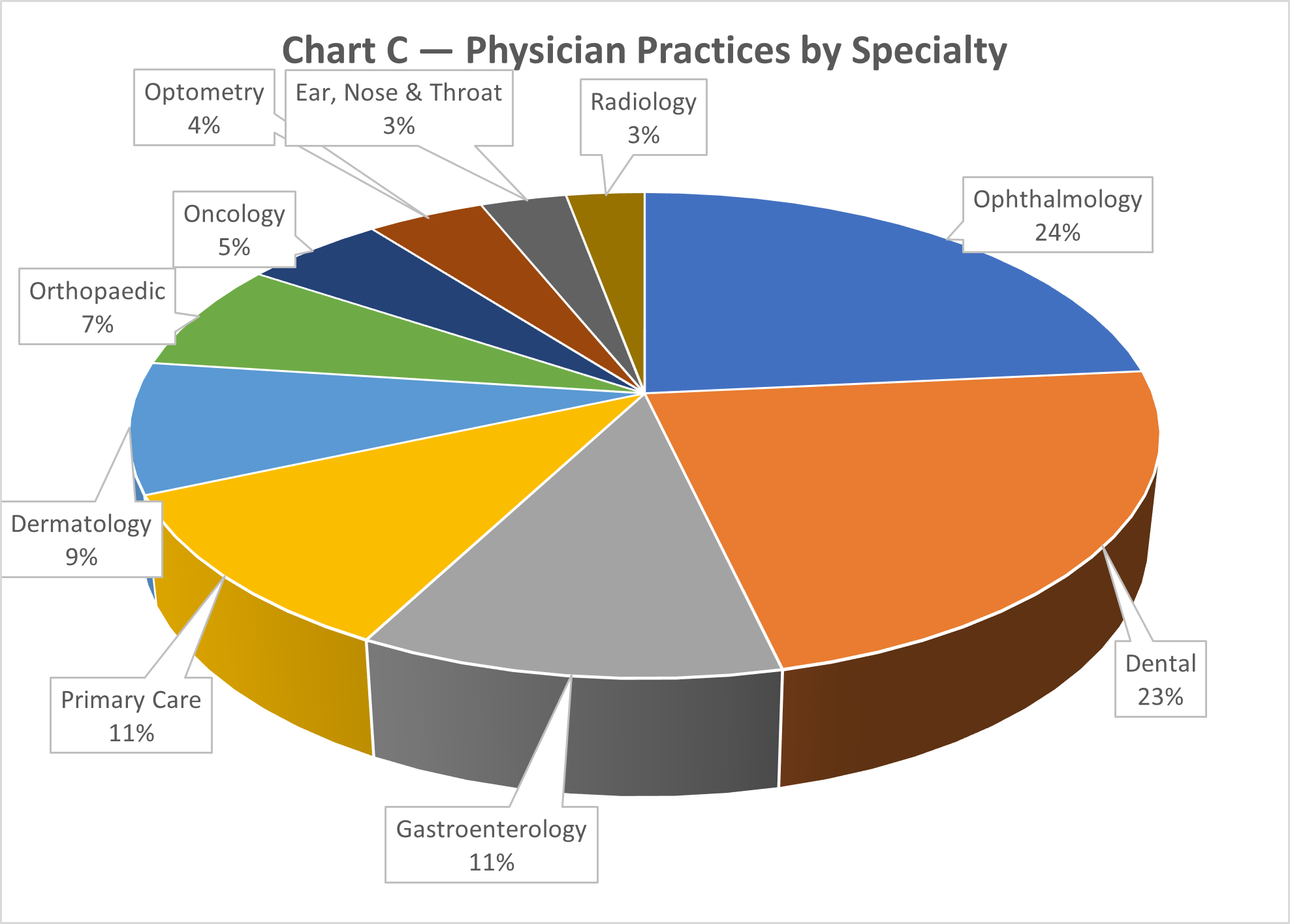

Physician practice management seeing an uptick in consolidation

After a cautious approach, deal making in the physician practice management market began its rebound in the fall of 2020. Investors started gaining insight into how practices were adapting to pandemic-related closures, including the use of telehealth and other technology-based means of serving patients.

Uncertainty around the future of the pandemic appears to have pushed some physician-owned practices to learn the pros and cons of private equity investment. Challenges involving recruitment and value-based payment caused many practices to consider management service organizations as a means of providing efficiencies of scale and reducing administrative burden — along with capital for growth and technology.

- Ophthalmology and dental practices are the most highly sought-after acquisition targets in recent years, based on volumes that are routinely “rolled up” through small practice acquisitions.

- The highly fragmented markets for these specialties — along with demand and a favorable payor mix — are driving demand in these segments.

- Private equity is the clear driver of consolidation, representing the majority of physician practice management transactions announced.

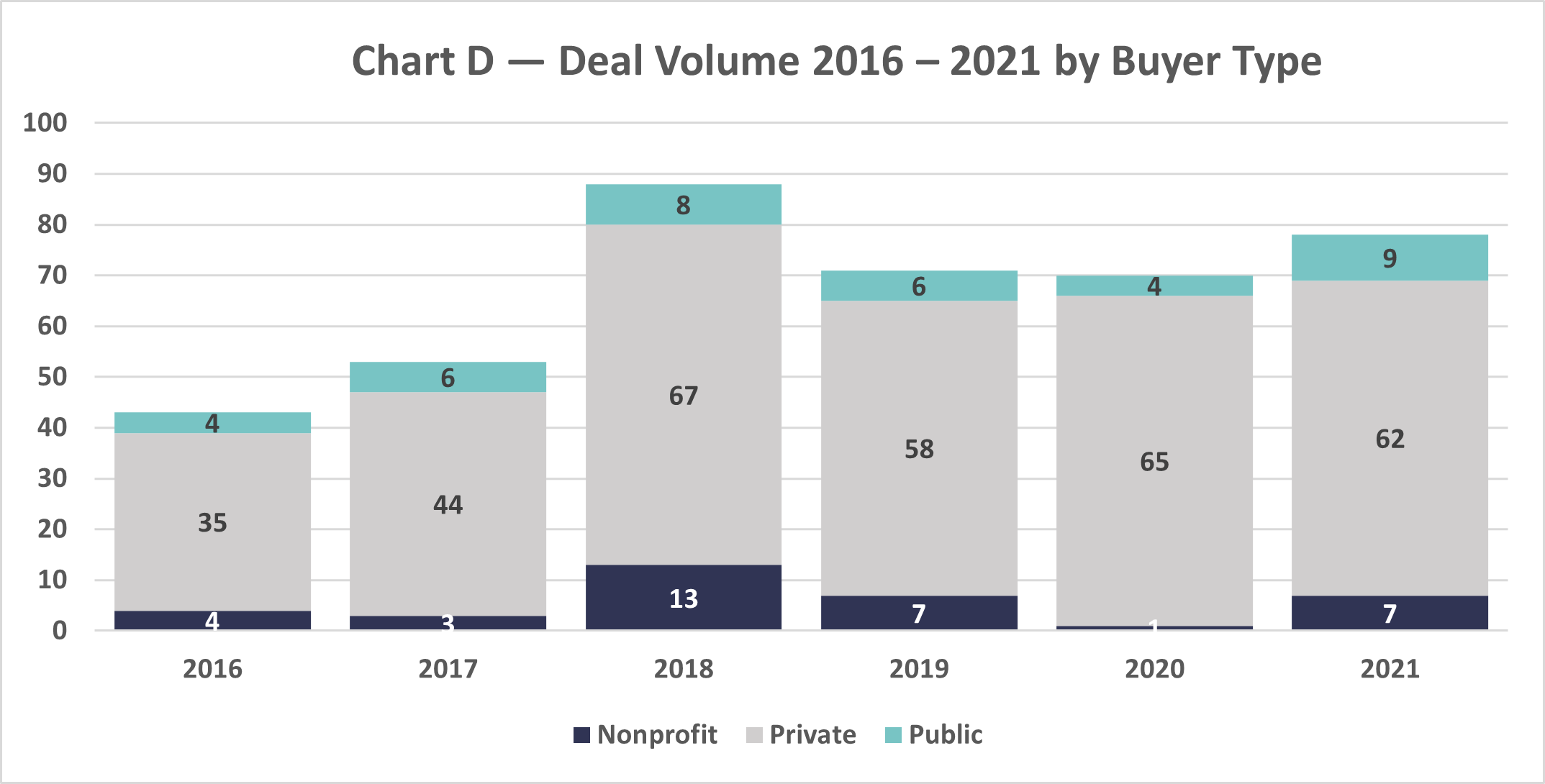

Long-term care transaction volume back to historically high levels

One of the health care segments most impacted by the pandemic is long-term care. Long-term care markets in Chart D include:

- Independent living communities and active adult

- Assisted living and memory care communities (AL/MC)

- Life plan communities

- Skilled nursing facilities (SNF)

Deal making slowed substantially in 2020 at the onset of COVID-19 and then began its rebound toward the end of the year. Despite intrinsic real estate challenges, transaction volumes appear to be back to historically high levels — likely due to significant levels of available capital. And the highest per unit/bed levels seen in years seem to be signaling confidence in the market.

These valuations are occurring while occupancy remains at historically low levels, particularly in the SNF market. High levels of provider relief funds received by SNF providers — and uncertainty surrounding continuing costs for personal protective equipment, infection control, and wages — can also make underwriting a challenge.

Within chart D, private equity looks to be leading the charge in deal activity. Though the pandemic revealed the industry’s heightened capacity to provide at-home care for elderly populations, investors remain bullish — primarily due to the unfolding demographic shift for coming years.

There appears to be an inverse relationship between risk and price — i.e., disclosed purchase prices indicate declining income capitalization rates indicating lower investor risk, which does not reflect the current economic uncertainty and risk profile of long-term care.

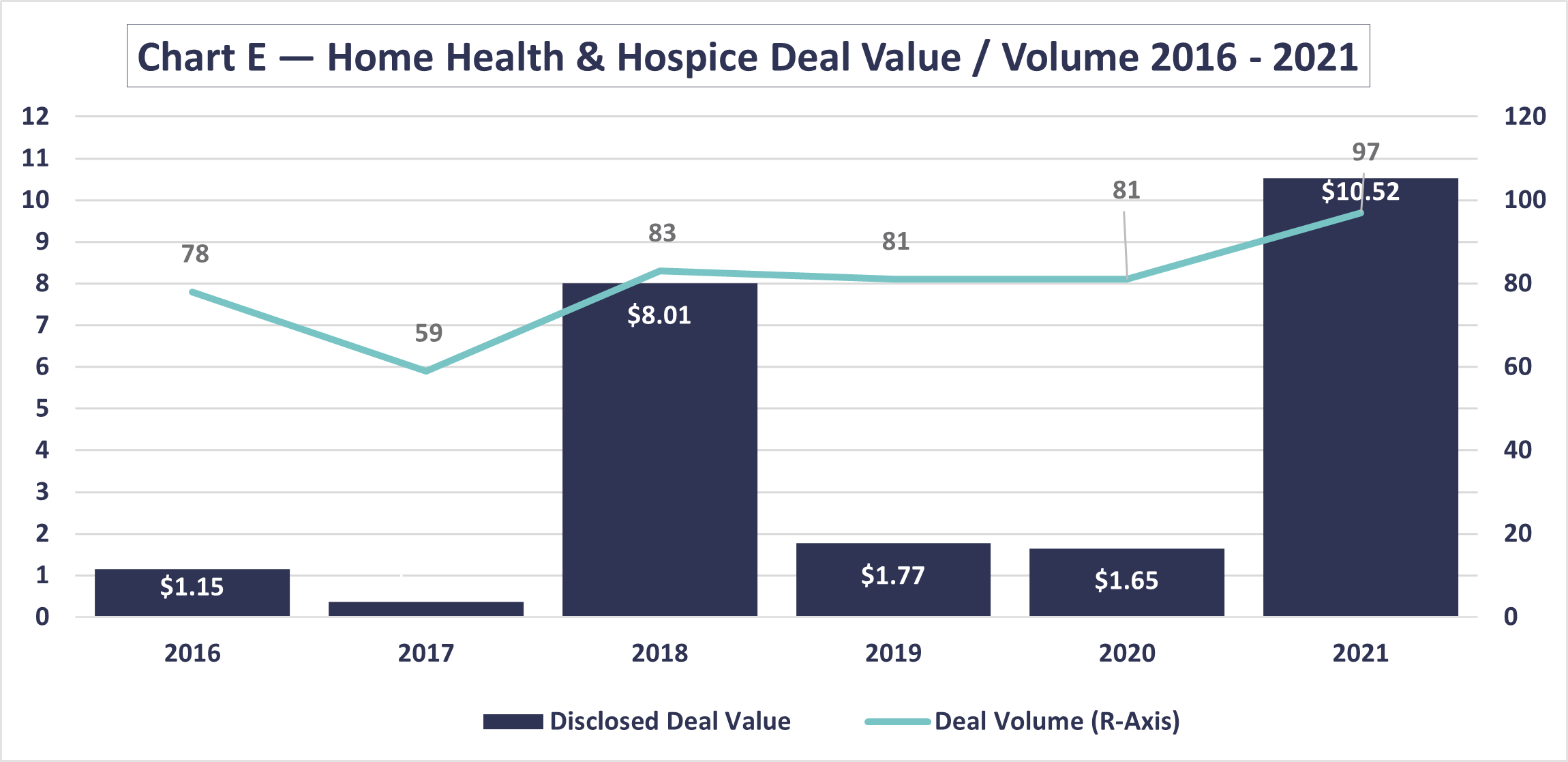

Home health and hospice segment transactions accelerating

Home health and hospice have seen some of the highest recorded valuation multiples in health care services. Though deal making halted following the onset of the pandemic, the market rebounded quickly in 2021, recording more transactions than any of the past five years (chart E).

The pandemic accelerated the emergent shift toward home care and community-based alternatives. Providers showed their ability to care for higher need populations in the home versus traditional settings, and had the opportunity to pose alternative care and payment models. In addition, prior to the COVID-19 pandemic, the shift from the Medicare payment model to the Payment Driven Groupings model caused uncertainty in cash flows, masked by pandemic complexities and the availability of provider relief funds.

As presented in chart E, private equity looks to be fueling deal growth — likely due to high levels of available capital, along with the attractiveness of the tailwinds related to government policy and a highly fragmented market. Many independently owned smaller agencies are at a significant disadvantage with the increasing regulation, and therefore may consider this the right time to sell.

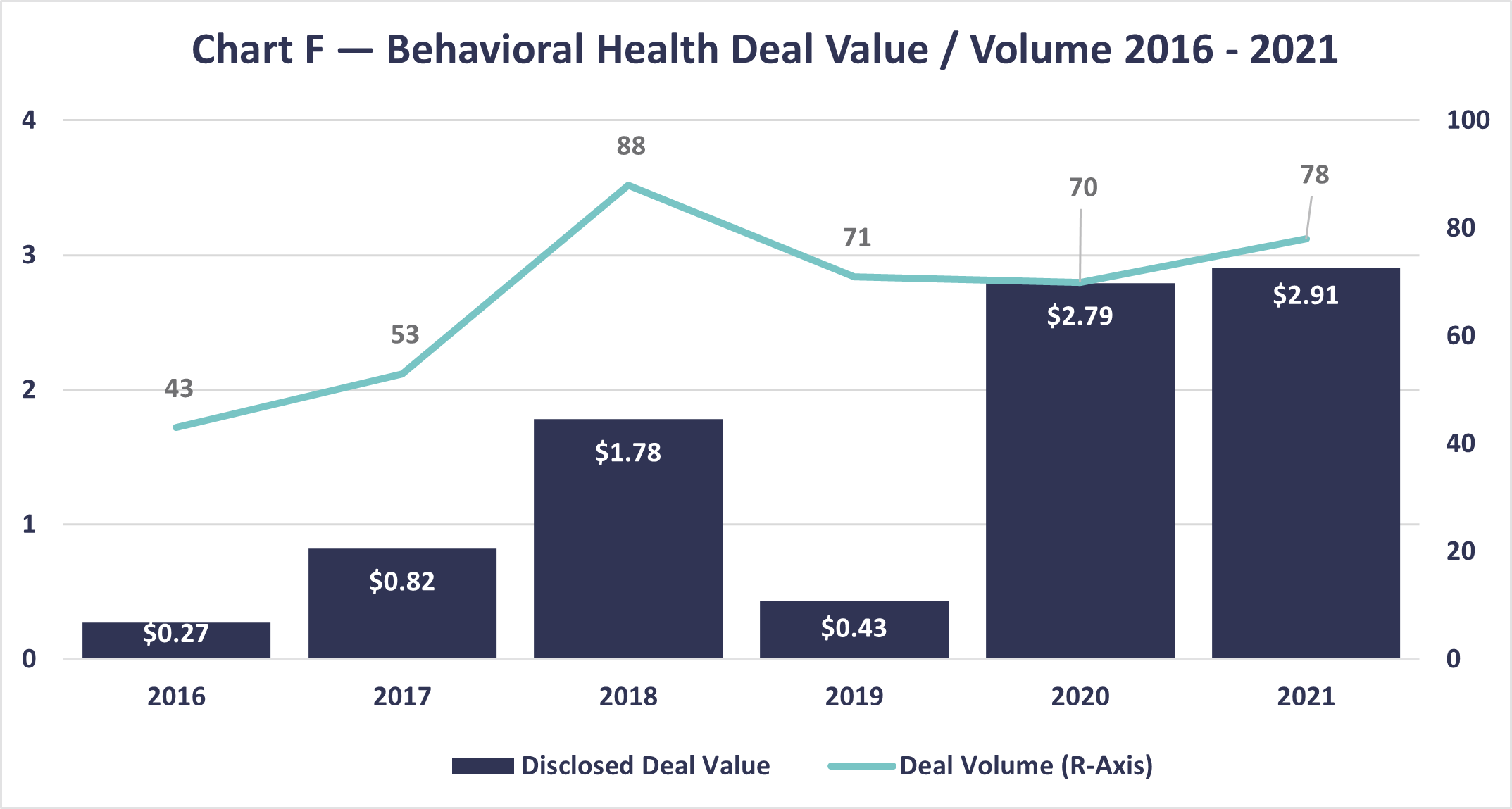

Behavioral health services in demand during the pandemic

Behavioral health has been edging into the spotlight in recent years and was further emphasized by the COVID-19 pandemic. Behavioral health consists of:

- Substance use (counseling, rehabilitation, medication-assisted treatment)

- Autism (autism treatment services)

- Intellectual and developmental disabilities (assistance with cognitive function and behavior)

- Eating disorders (eating behavior counseling)

- Counseling (health counseling / therapy)

- Inpatient behavioral (physical psychiatric hospital)

Outpatient substance use disorder, autism, and outpatient mental health appear to make up the majority of behavioral health transactions. Similar to other provider types, market fragmentation and projected consumer demand are key drivers of the consolidation.

The impact of technology on behavioral health services can’t be ignored. Telehealth was gaining traction prior to the pandemic and is now much more widely accepted. This increased access to care can be attractive to private equity investors and strategic buyers, as reflected in chart F.

How we can help

As we move through 2022, we anticipate seeing continued investment in innovative health care segments. However, deal making in the health care industry is adding to the complexities of the current climate. CLA goes beyond traditional accounting and financial analysis, and scrutinizes key assumptions underlying the deal — drawing on the deep health care experience of our dedicated health care transaction services team.

About the data

LevinPro HC and LevinPro LTC: The merger and acquisition data contained in various charts and tables in this report have been included only with the permission of the publisher, Irving Levin Associates LLC. All rights reserved.