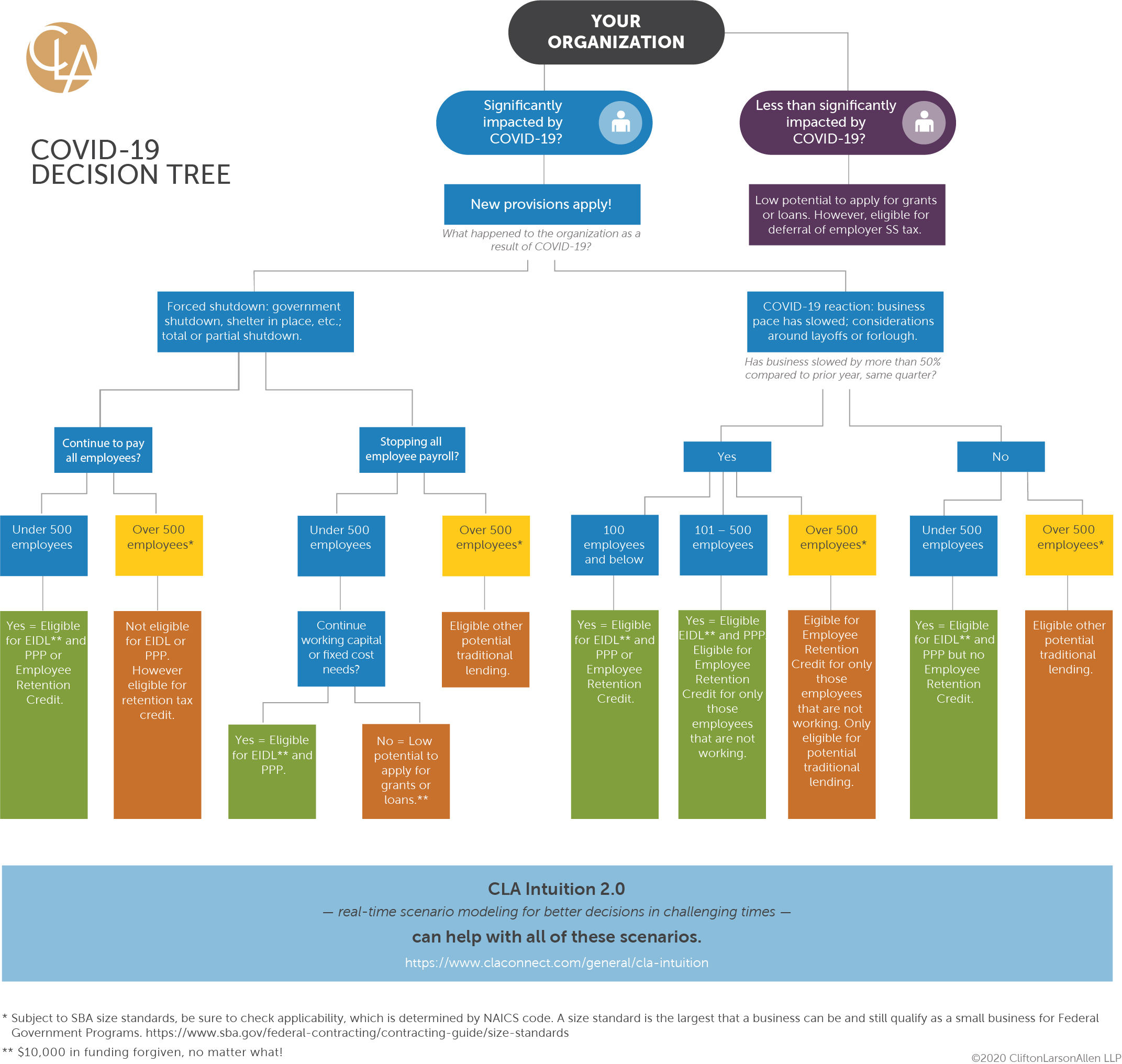

Forced shutdown or significant slowdown? Use our COVID-19 loan and grant decision tree to understand the options best suited for your organization.

Key insights

- The CARES Act expands EIDL and added a new Paycheck Protection Program (PPP) to the SBA’s lending program

- This adds up to tremendous opportunity for organizations to get the help they need

- Our decision tree can help guide you to your best path

Whether you’re considering Economic Injury Disaster Loan Assistance (EIDL), the Paycheck Protection Program (PPP), grants, or other financing, CLA is ready to help you find your way.

Navigate the options with our decision tree

[Click to enlarge]

Economic Injury Disaster Loan Assistance (EIDL)

Would you like to talk with an advisor?

The CARES Act expanded the U.S. Small Business Administration (SBA) EIDL program to provide SBA loans to qualified small businesses and other organizations.

- Qualifying organization can receive up to $2 million in loans to be used for working capital and ordinary expenditures.

- The actual amount available to any organization is tied to its economic injury from COVID-19 and will be determined by the SBA.

- Interest rates are 3.75% for small businesses and 2.75% for nonprofit organizations.

- EIDL loans are not forgivable, but eligible entities that apply for EIDL assistance can receive a $10,000 emergency grant within three days, even if the EIDL loan application is denied.

- An eligible organization is determined by the number of employees and average annual sales, with different standards per industry.

- Loans under this program are available to borrowers that can show they are unable to meet their existing financial obligations as a result of the COVID-19 crisis.

- Cannabis businesses, casinos, racetracks, and certain nonprofit organizations are among the entities that are not eligible.

Paycheck Protection Program (PPP)

PPP, created through the CARES Act, expands SBA support for eligible businesses and organizations, by offering loans of up to $10 million.

- Organizations that have been in existence for at least a year can obtain the lesser of 2.5 times their average monthly payroll for the previous 12 months, plus any amount refinanced from the EIDL assistance -or- $10 million.

- Entities not in existence for the previous 12 months can use their average monthly payroll for the period from January 1, 2020, through February 29, 2020.

- Funds can be used to cover payroll costs, rent and utilities, and interest on debt obligations.

- Funds cannot be used to compensate individual employees at an annual rate above $100,000, or to pay for emergency sick or family leave under the second coronavirus response package.

- Loans shall bear interest at a rate of 1%. For loans issued through June 30, 2020, payments of both principal and interest will be deferred for six months.

- Provided a company retains existing employees at or near current salary levels, the debt will be forgiven to the extent that proceeds are used in an eight-week period following loan origination for any of the following:

- Payroll costs and interest payments made on any mortgage or debt obligation incurred prior to February 15, 2020;

- Payment of any lease in force prior to February 15, 2020; and

- Payment on any utility under service agreements dated before February 15, 2020.

- The amount forgiven will be reduced by a formula that takes into consideration any reduction of workforce or wages. Additionally, forgiveness of non-payroll allowable expenses is limited to 25% of total forgiveness. Certain documentation is required to be retained, provided as proof, and certified to include with an application for loan forgiveness.

- Eligible recipients must meet one of the following requirements:

- 500 employees or fewer;

- Meet applicable employee size standards for their North American Industry Classification System (NAICS);

- 500 employees or fewer by location for those in the accommodation and food service industry (as defined by their NAICS code), or for any business acting as a franchise that is assigned a franchise identifier code by the SBA;

- Sole proprietors, independent contractors, and other self-employed individuals, including so-called gig economy workers; or

- Tax-exempt nonprofits under Section 501(c)(3) of 501(c)(19) of the Internal Revenue Code and tribal business concerns described in Section 31(b)(2)(C) of the Small Business Act.

Borrowers are precluded from receiving SBA funding under the PPP and an EIDL for the same purpose.

Loans for midsized businesses, states, and municipalities

The CARES Act authorizes a relief program, in an amount not to exceed $500 billion, that authorizes the Treasury to make loans, loan guarantees, and other investments in support of eligible businesses, states, and municipalities to address losses incurred as a result of coronavirus. This includes special assistance for eligible midsize organizations (500 to 10,000 employees).

- Annualized interest rate is not to exceed 2%.

- For the first six months (or longer, as the Treasury Secretary may determine), no principal or interest is due and payable.

- Loans are not forgivable.

- The act states that all eligible organizations that participate must make a good faith certification that:

- The uncertainty of the economic conditions as of the date of the application makes the loan request necessary to support the ongoing operations of the recipient.

- The recipient is an entity or business that is domiciled in the U.S. with significant operations and employees located in the U.S.

- The funds the recipient receives will be used to retain at least 90% of its workforce, at full compensation and benefits, until September 30, 2020.

- The recipient intends to restore not less than 90% of its workforce that existed as of February 1, 2020, and to restore all compensation and benefits to the workers of the recipient no later than four months after the termination of the public health emergency declared by the Secretary of Health and Human Services on January 31, 2020.

- The recipient is not a debtor in a bankruptcy proceeding.

- While the direct loan is outstanding, the recipient will not pay dividends with respect to the common stock of the eligible business or purchase an equity security that is listed on a national securities exchange of the recipient or any parent company of the recipient, except to the extent required under a contractual obligation that was in effect as of the date of on which the CARES Act was enacted.

- The recipient will not outsource offshore jobs for the term of the loan and two years after completing repayment of the loan.

- The recipient will not repeal existing collective bargaining agreements for the term of the loan and two years after completing repayment of the loan, and will remain neutral in any union organizing effort for the term of the loan.

Application processes for these midsize organization loans are not yet available.

How we can help

We’re here to help you through this complex, rapidly changing environment. We will work together with you to understand your unique situation, strategize on immediate decisions, and help you to pull together the information necessary for you to submit your loan application.